Peer Review Changes/Revisions Related to A-133 Engagements

|

|

|

- Cameron Underwood

- 5 years ago

- Views:

Transcription

1 Peer Review Changes/Revisions Related to A-133 Engagements Peer Review Changes/Revisions Related to A-133 Engagements Jim Brackens, CPA, AICPA, VP - Firm Quality and Practice Monitoring David Jentho, CPA, Chair, AICPA Practice Monitoring Task Force Nancy Miller, CPA, Chair, AICPA Technical Standards Subcommittee Governmental Group (Ethics)

2 Topics for Today s Conference Call Single Audit Quality Concerns (PCIE Report) AICPA Response Revisions to Peer Review Standards Interpretation 63-1a Revisions to Single Audit Checklist and Engagement Profiles for Not-for-Profit and Governmental Engagements Additional Changes under Consideration by PRB 2

3 Questions during the call any questions or comments during the call to the Peer Review Technical mail box: Include your name and phone number if you are willing to discuss your question on the call 3

4 Single Audit Quality Concerns (PCIE Report) Scope: June 2007 PCIE Report covered 208 out of 38,000 single audits performed in 2002/2003 Report Results/Concerns: Acceptable 49% Unacceptable/Limited reliability 51% Findings: PCIE Reports Areas of Improvements Needed Internal control, compliance, documentation, sampling, due professional care 4

Failure to test all major programs within clusters Not including all grants within a CFDA # Internal control documentation")

5 Single Audit Quality Concerns (PCIE Report) Frequent Single Audit Violations Major program determination (missed major program look back rule) Percent of coverage Incorrect threshold for major program determination Improper identification of clusters (missing programs) Failure to test all major programs within clusters Not including all grants within a CFDA # Internal control documentation and compliance testing 5

Pre-requisite and continuing training for staff conducting single audits 6")

6 PCIE Recommendations OMB commitment to work with AICPA, NASBA and other similar organizations to address PCIE recommendations Revise and improve Single Audit Standards, criteria, and guidance Enhance documentation requirements, including sample sizes for compliance testing (SAS 39) Pre-requisite and continuing training for staff conducting single audits 6

7 Impact on AICPA and Peer Review Specific mention of AICPA responsibility in PCIE report Congressional testimony by AICPA Potential repercussions for continued unacceptable single audits Governmental Audit Quality Center Recent GAQC Call: The Recovery Act: A Practitioner's Perspective (will be archived on the GAQC website within 2 weeks) 7

8 AICPA Response AICPA developed seven task forces to examine the PCIE study's detailed findings and make recommendations as follows: Sampling/Materiality Issues In A Single Audit Environment Internal Control And Compliance Responsibilities In A Single Audit Environment Schedule Of Expenditures of Federal Awards Reporting Issues Reporting Audit Findings In A Single Audit Single Audit Training Needs And Continuing Professional Education Evaluation Practice Monitoring In A Single Audit Environment Compliance Auditing Considerations In Audits Of Governmental Entities And Recipients Of Governmental Financial Assistance 8

9 Practice Monitoring Task Force (PMTF) Areas of Focus: Establish consistent measures of A-133 deficiencies Develop guidance and training materials for peer reviewers Task Force Activities: Meeting with OIGs to discuss Peer Review process and comparing to QCR process Brainstorming session to consider comments and recommendations received from IGs 9

10 PMTF Actions Taken Interpretation 63-1a revised to require selection of an A-133 engagement Revision to Interpretation 63-1a (June 2009 Peer Review Alert) Effective for peer reviews commencing on or after September 1, 2009 Must-selects must include A-133 engagements No further modification to System Report mustselect paragraph 10

has revised this interpretation to require that additionally, if the engagement selected is of an entity subject to GAS but not subject to the Single Audit Act/OMB")

11 Revised Interpretation 63-1a Peer Review Standards Interpretation 63-1a has been updated. The Peer Review Board (PRB) has revised this interpretation to require that additionally, if the engagement selected is of an entity subject to GAS but not subject to the Single Audit Act/OMB Circular A-133 and the firm performs engagements of entities subject to OMB Circular A-133, at least one such engagement should also be selected for review. 11

PRP")

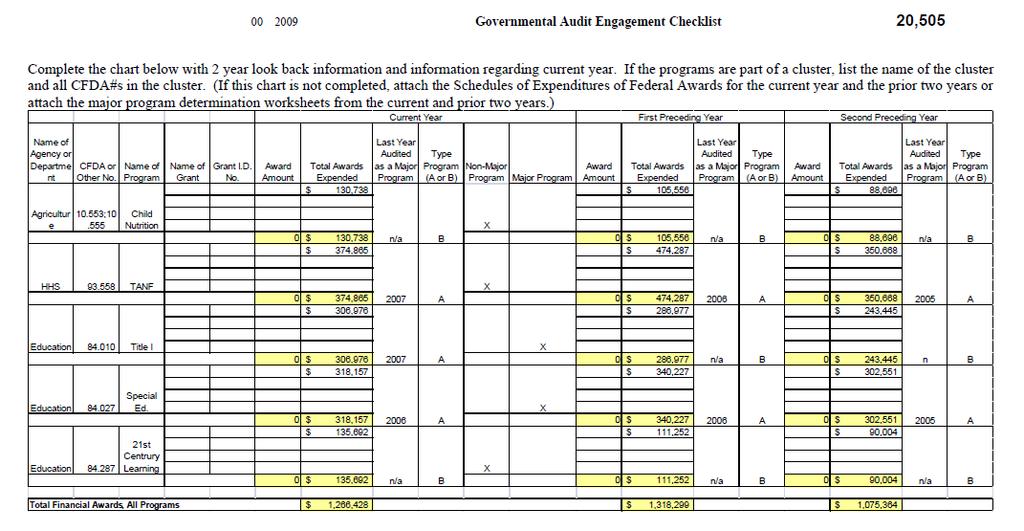

12 Revised Governmental and Not-For-Profit Audit Engagement Checklist (and Engagement Profiles) PRP Manual Section 20, 500 and 20,600 Enhanced key A-133 Single Audit Data Single Audit Major Program Determination worksheet 12

13 13

14 14

15 Part A & B Single Audit/A-133 Supplemental Checklists (Mandatory use effective for peer reviews commencing November 1, 2009 and after) Part A Supplemental Checklist for Review of Single Audit Act/A-133 Engagements PRP Manual Section 22100A Begin with Part A Checklist Addresses most problematic concerns Determination of major programs Audit of major programs Audit findings Schedule of Expenditures of Federal Awards 15

Not required to further complete Part A nor Part B once reviewer reaches conclusion of failed engagement")

16 Part A & B Single Audit/A-133 Supplemental Checklists Complete Part A until a question answered No -- confirms engagement not performed in conformity with applicable professional standards in all material respects (Inspectors General consider these failures make engagement unacceptable ) Not required to further complete Part A nor Part B once reviewer reaches conclusion of failed engagement Document decision Consider expanding scope of peer review as applicable (PRP Standards Section 1000 par. 68) 16

17 17

18 Part A & B Single Audit/A-133 Supplemental Checklists Part B Supplemental Checklist for Review of Single Audit Act/A-133 Engagements PRP Manual Section 22100B Report on Compliance Schedule of Findings and Questioned Costs Other Audit Issues and Program Specific Audits Failure in one of these areas does not necessarily result in an engagement that has not been performed in accordance with GAGAS in all material respects 18

19 Failure to Meet Coverage Percent for High Risk Auditee 19

20 Example of a Missed Major Program 20

21 Potential Concerns About New Engagement Profile and Supplemental Checklists Reviewed firm completes Engagement Profile and Major Program Determination - minimal data requested that should be easily ascertained and documented. Major Program Determination Worksheet - template provided or use auditor s determination worksheet IF it provides all of the same information, including lookback information. Part A&B Checklists include minimal (5) new questions; otherwise just split out of existing Single Audit/A-133 Supplemental Checklist. Part A&B Checklist format should save peer reviewers time. 21

22 PMTF Direction and Considerations Recommended Enhanced Peer Review Report Acceptance and Oversight Procedure Changes Engagement Profile and Part A Supplemental A-133 Checklist evaluated by Technical Reviewer and/or RAB as part of report acceptance procedure Timeline Concerns about the new process: Required subject matter expertise and experience by Technical Reviewers and Report Acceptance Bodies Consideration of national pool of A-133 subject matter experts for consultations and to provide technical advice Enhanced RAB responsibilities 22

23 Questions, Comments or Suggestions? any questions or comments during the call to the Peer Review Technical mail box: Include your name and phone number if you are willing to discuss your question on the call 23

24 Thank you! 24

2013 Peer Review Conference. Providence, RI. Committee Member Session: Topics and Questions for Discussion

2013 Peer Review Conference Providence, RI Committee Member Session: Topics and Questions for Discussion 1 TABLE OF CONTENTS FOR COMMITTEE MEMBER SESSION TOPIC # TOPIC DESCRIPTION PAGE # 1 Clarified Auditing

2013 Peer Review Conference Providence, RI Committee Member Session: Topics and Questions for Discussion 1 TABLE OF CONTENTS FOR COMMITTEE MEMBER SESSION TOPIC # TOPIC DESCRIPTION PAGE # 1 Clarified Auditing

Audit Documentation. This redrafted SSA 230 supersedes the SSA of the same title in April 2008.

SINGAPORE STANDARD ON AUDITING SSA 230 Audit Documentation This redrafted SSA 230 supersedes the SSA of the same title in April 2008. This SSA has been updated in January 2010 following a clarity consistency

SINGAPORE STANDARD ON AUDITING SSA 230 Audit Documentation This redrafted SSA 230 supersedes the SSA of the same title in April 2008. This SSA has been updated in January 2010 following a clarity consistency

Differential Tuition Budget Proposal FY

Differential Tuition Budget Proposal FY 2013-2014 MPA Differential Tuition Subcommittee MPA Faculty This document presents the budget proposal of the MPA Differential Tuition Subcommittee (MPADTS) for

Differential Tuition Budget Proposal FY 2013-2014 MPA Differential Tuition Subcommittee MPA Faculty This document presents the budget proposal of the MPA Differential Tuition Subcommittee (MPADTS) for

"iake R TI LL Y. January 29,2016

"iake R TI LL Y January 29,2016 Baker Tilly Virchow Krause, LLP 225 S Sixth St, Ste 2300 Minneapolis, MN 55402-4661 tel 612 8764500 fax 612 238 8900 bakerrilly.corn Ms. Rachelle Drummond Senior Technical

"iake R TI LL Y January 29,2016 Baker Tilly Virchow Krause, LLP 225 S Sixth St, Ste 2300 Minneapolis, MN 55402-4661 tel 612 8764500 fax 612 238 8900 bakerrilly.corn Ms. Rachelle Drummond Senior Technical

Pro Bono Practices and Opportunities in Mexico

Pro Bono Practices and Opportunities in Mexico Excerpt from: A Survey of Pro Bono Practices and Opportunities in Selected Jurisdictions September 2010 Prepared by Latham & Watkins LLP for the Pro Bono

Pro Bono Practices and Opportunities in Mexico Excerpt from: A Survey of Pro Bono Practices and Opportunities in Selected Jurisdictions September 2010 Prepared by Latham & Watkins LLP for the Pro Bono

Montana Board of Public Accountants

Montana Board of Public Accountants In This Issue A Look at the New Officers...2 Reporting Peer Review...2 Annual Firm Registration...2 New Uniform CPA Exam Practice Anaylsis...3 CPEtracker...3 Future

Montana Board of Public Accountants In This Issue A Look at the New Officers...2 Reporting Peer Review...2 Annual Firm Registration...2 New Uniform CPA Exam Practice Anaylsis...3 CPEtracker...3 Future

Consent for Further Education Colleges to Invest in Companies September 2011

Consent for Further Education Colleges to Invest in Companies September 2011 Of interest to college principals and finance directors as well as staff within the Skills Funding Agency. Summary This guidance

Consent for Further Education Colleges to Invest in Companies September 2011 Of interest to college principals and finance directors as well as staff within the Skills Funding Agency. Summary This guidance

M.S. in Environmental Science Graduate Program Handbook. Department of Biology, Geology, and Environmental Science

M.S. in Environmental Science Graduate Program Handbook Department of Biology, Geology, and Environmental Science Welcome Welcome to the Master of Science in Environmental Science (M.S. ESC) program offered

M.S. in Environmental Science Graduate Program Handbook Department of Biology, Geology, and Environmental Science Welcome Welcome to the Master of Science in Environmental Science (M.S. ESC) program offered

HOUSE OF REPRESENTATIVES AS REVISED BY THE COMMITTEE ON EDUCATION APPROPRIATIONS ANALYSIS

BILL #: HB 269 HOUSE OF REPRESENTATIVES AS REVISED BY THE COMMITTEE ON EDUCATION APPROPRIATIONS ANALYSIS RELATING TO: SPONSOR(S): School District Best Financial Management Practices Reviews Representatives

BILL #: HB 269 HOUSE OF REPRESENTATIVES AS REVISED BY THE COMMITTEE ON EDUCATION APPROPRIATIONS ANALYSIS RELATING TO: SPONSOR(S): School District Best Financial Management Practices Reviews Representatives

State Parental Involvement Plan

A Toolkit for Title I Parental Involvement Section 3 Tools Page 41 Tool 3.1: State Parental Involvement Plan Description This tool serves as an example of one SEA s plan for supporting LEAs and schools

A Toolkit for Title I Parental Involvement Section 3 Tools Page 41 Tool 3.1: State Parental Involvement Plan Description This tool serves as an example of one SEA s plan for supporting LEAs and schools

MSW POLICY, PLANNING & ADMINISTRATION (PP&A) CONCENTRATION

CONCENTRATION") MSW POLICY, PLANNING & ADMINISTRATION (PP&A) CONCENTRATION Overview of the Policy, Planning, and Administration Concentration Policy, Planning, and Administration Concentration Goals and Objectives Policy,

MSW POLICY, PLANNING & ADMINISTRATION (PP&A) CONCENTRATION Overview of the Policy, Planning, and Administration Concentration Policy, Planning, and Administration Concentration Goals and Objectives Policy,

Office of Inspector General The School District of Palm Beach County

Office of Inspector General The School District of Palm Beach County Case No. 16 431 Payments to Soccer Referees INVESTIGATIVE REPORT AUTHORITY School Board Policy 1.092, Inspector General (4)(a)(iv) provides

Office of Inspector General The School District of Palm Beach County Case No. 16 431 Payments to Soccer Referees INVESTIGATIVE REPORT AUTHORITY School Board Policy 1.092, Inspector General (4)(a)(iv) provides

1 Use complex features of a word processing application to a given brief. 2 Create a complex document. 3 Collaborate on a complex document.

National Unit specification General information Unit code: HA6M 46 Superclass: CD Publication date: May 2016 Source: Scottish Qualifications Authority Version: 02 Unit purpose This Unit is designed to

National Unit specification General information Unit code: HA6M 46 Superclass: CD Publication date: May 2016 Source: Scottish Qualifications Authority Version: 02 Unit purpose This Unit is designed to

AB104 Adult Education Block Grant. Performance Year:

AB104 Adult Education Block Grant Performance Year: 2015-2016 Funding source: AB104, Section 39, Article 9 Version 1 Release: October 9, 2015 Reporting & Submission Process Required Funding Recipient Content

AB104 Adult Education Block Grant Performance Year: 2015-2016 Funding source: AB104, Section 39, Article 9 Version 1 Release: October 9, 2015 Reporting & Submission Process Required Funding Recipient Content

Assessment Pack HABC Level 3 Award in Education and Training (QCF)

") www.highfieldabc.com Assessment Pack HABC Level 3 Award in Education and Training (QCF) Version 1: December 2013 Contents Introduction 3 Learner Details 5 Centre Details 5 Achievement Summary Sheet 6 Declaration

www.highfieldabc.com Assessment Pack HABC Level 3 Award in Education and Training (QCF) Version 1: December 2013 Contents Introduction 3 Learner Details 5 Centre Details 5 Achievement Summary Sheet 6 Declaration

A Profile of Top Performers on the Uniform CPA Exam

Marquette University e-publications@marquette Accounting Faculty Research and Publications Business Administration, College of 8-1-2014 A Profile of Top Performers on the Uniform CPA Exam Michael D. Akers

Marquette University e-publications@marquette Accounting Faculty Research and Publications Business Administration, College of 8-1-2014 A Profile of Top Performers on the Uniform CPA Exam Michael D. Akers

Office: Gallagher Hall 3406

Accounting Ethics (ACC 271) Graduate School of Management University of California at Davis Professor Robert Yetman Fall 2012 Thursdays 12:00 noon - 4:00pm Email: rjyetman@ucdavis.edu Office: Gallagher

Accounting Ethics (ACC 271) Graduate School of Management University of California at Davis Professor Robert Yetman Fall 2012 Thursdays 12:00 noon - 4:00pm Email: rjyetman@ucdavis.edu Office: Gallagher

ACC 362 Course Syllabus

ACC 362 Course Syllabus Unique 02420, MWF 1-2 Fall 2005 Faculty Information Lecturer: Lynn Serre Dikolli Office: GSB 5.124F Voice: 232-9343 Office Hours: MW 9.30-10.30, F 12-1 other times by appointment

ACC 362 Course Syllabus Unique 02420, MWF 1-2 Fall 2005 Faculty Information Lecturer: Lynn Serre Dikolli Office: GSB 5.124F Voice: 232-9343 Office Hours: MW 9.30-10.30, F 12-1 other times by appointment

Class Numbers: & Personal Financial Management. Sections: RVCC & RVDC. Summer 2008 FIN Fully Online

Summer 2008 FIN 3140 Personal Financial Management Fully Online Sections: RVCC & RVDC Class Numbers: 53262 & 53559 Instructor: Jim Keys Office: RB 207B, University Park Campus Office Phone: 305-348-3268

Summer 2008 FIN 3140 Personal Financial Management Fully Online Sections: RVCC & RVDC Class Numbers: 53262 & 53559 Instructor: Jim Keys Office: RB 207B, University Park Campus Office Phone: 305-348-3268

2. Related Documents (refer to policies.rutgers.edu for additional information)

") Policy Name: Clinical Affiliation Agreements Approval Authority: RBHS Chancellor Originally Issued: Revisions: 6/20/13 1. Who Should Read This Policy All Rutgers University research faculty and staff within

Policy Name: Clinical Affiliation Agreements Approval Authority: RBHS Chancellor Originally Issued: Revisions: 6/20/13 1. Who Should Read This Policy All Rutgers University research faculty and staff within

Higher Education Review (Embedded Colleges) of Kaplan International Colleges UK Ltd

of Kaplan International Colleges UK Ltd") Higher Education Review (Embedded Colleges) of Kaplan International Colleges UK Ltd June 2016 Contents About this review... 1 Key findings... 2 QAA's judgements about Kaplan International Colleges UK Ltd...

Higher Education Review (Embedded Colleges) of Kaplan International Colleges UK Ltd June 2016 Contents About this review... 1 Key findings... 2 QAA's judgements about Kaplan International Colleges UK Ltd...

CHAPTER XI DIRECT TESTIMONY OF REGINALD M. AUSTRIA ON BEHALF OF SOUTHERN CALIFORNIA GAS COMPANY AND SAN DIEGO GAS & ELECTRIC COMPANY

Application No: A.1-09-00 Exhibit No.: Witness: R. Austria Application of Southern California Gas Company (U 90 G) and San Diego Gas & Electric Company (U 90 G) to Recover Costs Recorded in the Pipeline

Application No: A.1-09-00 Exhibit No.: Witness: R. Austria Application of Southern California Gas Company (U 90 G) and San Diego Gas & Electric Company (U 90 G) to Recover Costs Recorded in the Pipeline

CORE CURRICULUM FOR REIKI

CORE CURRICULUM FOR REIKI Published July 2017 by The Complementary and Natural Healthcare Council (CNHC) copyright CNHC Contents Introduction... page 3 Overall aims of the course... page 3 Learning outcomes

CORE CURRICULUM FOR REIKI Published July 2017 by The Complementary and Natural Healthcare Council (CNHC) copyright CNHC Contents Introduction... page 3 Overall aims of the course... page 3 Learning outcomes

Introduction 3. Outcomes of the Institutional audit 3. Institutional approach to quality enhancement 3

De Montfort University March 2009 Annex to the report Contents Introduction 3 Outcomes of the Institutional audit 3 Institutional approach to quality enhancement 3 Institutional arrangements for postgraduate

De Montfort University March 2009 Annex to the report Contents Introduction 3 Outcomes of the Institutional audit 3 Institutional approach to quality enhancement 3 Institutional arrangements for postgraduate

Quality assurance of Authority-registered subjects and short courses

Quality assurance of Authority-registered subjects and short courses 170133 The State of Queensland () 2017 PO Box 307 Spring Hill QLD 4004 Australia 154 Melbourne Street, South Brisbane Phone: (07) 3864

Quality assurance of Authority-registered subjects and short courses 170133 The State of Queensland () 2017 PO Box 307 Spring Hill QLD 4004 Australia 154 Melbourne Street, South Brisbane Phone: (07) 3864

Unit 3. Design Activity. Overview. Purpose. Profile

Unit 3 Design Activity Overview Purpose The purpose of the Design Activity unit is to provide students with experience designing a communications product. Students will develop capability with the design

Unit 3 Design Activity Overview Purpose The purpose of the Design Activity unit is to provide students with experience designing a communications product. Students will develop capability with the design

Procedures for Academic Program Review. Office of Institutional Effectiveness, Academic Planning and Review

Procedures for Academic Program Review Office of Institutional Effectiveness, Academic Planning and Review Last Revision: August 2013 1 Table of Contents Background and BOG Requirements... 2 Rationale

Procedures for Academic Program Review Office of Institutional Effectiveness, Academic Planning and Review Last Revision: August 2013 1 Table of Contents Background and BOG Requirements... 2 Rationale

University of Michigan - Flint POLICY ON FACULTY CONFLICTS OF INTEREST AND CONFLICTS OF COMMITMENT

University of Michigan - Flint POLICY ON FACULTY CONFLICTS OF INTEREST AND CONFLICTS OF COMMITMENT A. Identification of Potential Conflicts of Interest and Commitment Potential conflicts of interest and

University of Michigan - Flint POLICY ON FACULTY CONFLICTS OF INTEREST AND CONFLICTS OF COMMITMENT A. Identification of Potential Conflicts of Interest and Commitment Potential conflicts of interest and

content First Introductory book to cover CAPM First to differentiate expected and required returns First to discuss the intrinsic value of stocks

content First Introductory book to cover CAPM First to differentiate expected and required returns First to discuss the intrinsic value of stocks presentation First timelines to explain TVM First financial

content First Introductory book to cover CAPM First to differentiate expected and required returns First to discuss the intrinsic value of stocks presentation First timelines to explain TVM First financial

ACC 380K.4 Course Syllabus

ACC 380K.4 Course Syllabus Unique 02485, MW 11-12.30 Fall 2005 Faculty Information Lecturer: Lynn Serre Dikolli Office: GSB 5.124F Voice: 232-9343 Office Hours: MW 9.30-10.30, F 12-1 other times by appointment

ACC 380K.4 Course Syllabus Unique 02485, MW 11-12.30 Fall 2005 Faculty Information Lecturer: Lynn Serre Dikolli Office: GSB 5.124F Voice: 232-9343 Office Hours: MW 9.30-10.30, F 12-1 other times by appointment

Reference to Tenure track faculty in this document includes tenured faculty, unless otherwise noted.

PHILOSOPHY DEPARTMENT FACULTY DEVELOPMENT and EVALUATION MANUAL Approved by Philosophy Department April 14, 2011 Approved by the Office of the Provost June 30, 2011 The Department of Philosophy Faculty

PHILOSOPHY DEPARTMENT FACULTY DEVELOPMENT and EVALUATION MANUAL Approved by Philosophy Department April 14, 2011 Approved by the Office of the Provost June 30, 2011 The Department of Philosophy Faculty

REPORT OF THE PROVOST S REVIEW PANEL. Clinical Practices and Research in the Department of Neurological Surgery June 27, 2013

REPORT OF THE PROVOST S REVIEW PANEL Clinical Practices and Research in the Department of Neurological Surgery June 27, 2013 Executive Summary In August 2012 the Provost and Executive Vice Chancellor convened

REPORT OF THE PROVOST S REVIEW PANEL Clinical Practices and Research in the Department of Neurological Surgery June 27, 2013 Executive Summary In August 2012 the Provost and Executive Vice Chancellor convened

UTILITY POLE ATTACHMENTS Understanding New FCC Regulations and Industry Trends

COURSE UTILITY POLE ATTACHMENTS Understanding New FCC Regulations and Industry Trends May 1-2, 2017 Atlanta Marriott Suites Midtown Atlanta, GA EUCI is authorized by IACET to offer 1.0 CEUs for this course

COURSE UTILITY POLE ATTACHMENTS Understanding New FCC Regulations and Industry Trends May 1-2, 2017 Atlanta Marriott Suites Midtown Atlanta, GA EUCI is authorized by IACET to offer 1.0 CEUs for this course

1. Faculty responsible for teaching those courses for which a test is being used as a placement tool.

Studies Addressing Content-Related Validity Materials needed 1. A listing of prerequisite knowledge and skills for each of the courses for which a test is being used as a placement tool, i.e., identify

Studies Addressing Content-Related Validity Materials needed 1. A listing of prerequisite knowledge and skills for each of the courses for which a test is being used as a placement tool, i.e., identify

Massachusetts Department of Elementary and Secondary Education. Title I Comparability

Massachusetts Department of Elementary and Secondary Education Title I Comparability 2009-2010 Title I provides federal financial assistance to school districts to provide supplemental educational services

Massachusetts Department of Elementary and Secondary Education Title I Comparability 2009-2010 Title I provides federal financial assistance to school districts to provide supplemental educational services

Definitions for KRS to Committee for Mathematics Achievement -- Membership, purposes, organization, staffing, and duties

158.842 Definitions for KRS 158.840 to 158.844 -- Committee for Mathematics Achievement -- Membership, purposes, organization, staffing, and duties of committee -- Report to Interim Joint Committee on

158.842 Definitions for KRS 158.840 to 158.844 -- Committee for Mathematics Achievement -- Membership, purposes, organization, staffing, and duties of committee -- Report to Interim Joint Committee on

Academic Affairs Policy #1

Academic Affairs Policy #1 Academic Institutes and Centers Date of Current Revision: April 2017 Responsible Office: Vice Provost for Research and Scholarship 1. PURPOSE This policy provides guidelines

Academic Affairs Policy #1 Academic Institutes and Centers Date of Current Revision: April 2017 Responsible Office: Vice Provost for Research and Scholarship 1. PURPOSE This policy provides guidelines

TITLE IX COMPLIANCE SAN DIEGO STATE UNIVERSITY. Audit Report June 14, Henry Mendoza, Chair Steven M. Glazer William Hauck Glen O.

TITLE IX COMPLIANCE SAN DIEGO STATE UNIVERSITY Audit Report 12-18 June 14, 2012 Henry Mendoza, Chair Steven M. Glazer William Hauck Glen O. Toney Members, Committee on Audit University Auditor: Larry Mandel

TITLE IX COMPLIANCE SAN DIEGO STATE UNIVERSITY Audit Report 12-18 June 14, 2012 Henry Mendoza, Chair Steven M. Glazer William Hauck Glen O. Toney Members, Committee on Audit University Auditor: Larry Mandel

5 Early years providers

5 Early years providers What this chapter covers This chapter explains the action early years providers should take to meet their duties in relation to identifying and supporting all children with special

5 Early years providers What this chapter covers This chapter explains the action early years providers should take to meet their duties in relation to identifying and supporting all children with special

PREPARING FOR THE SITE VISIT IN YOUR FUTURE

PREPARING FOR THE SITE VISIT IN YOUR FUTURE ARC-PA Suzanne York SuzanneYork@arc-pa.org 2016 PAEA Education Forum Minneapolis, MN Saturday, October 15, 2016 TODAY S SESSION WILL INCLUDE: Recommendations

PREPARING FOR THE SITE VISIT IN YOUR FUTURE ARC-PA Suzanne York SuzanneYork@arc-pa.org 2016 PAEA Education Forum Minneapolis, MN Saturday, October 15, 2016 TODAY S SESSION WILL INCLUDE: Recommendations

Bethune-Cookman University

Bethune-Cookman University The Independent Colleges and Universities of Florida Community College Articulation Manual 2012-2013 1 BETHUNE-COOKMAN UNIVERSITY ICUF ARTICULATION MANUAL GENERAL ADMISSION PROCEDURES

Bethune-Cookman University The Independent Colleges and Universities of Florida Community College Articulation Manual 2012-2013 1 BETHUNE-COOKMAN UNIVERSITY ICUF ARTICULATION MANUAL GENERAL ADMISSION PROCEDURES

Rules of Procedure for Approval of Law Schools

Rules of Procedure for Approval of Law Schools Table of Contents I. Scope and Authority...49 Rule 1: Scope and Purpose... 49 Rule 2: Council Responsibility and Authority with Regard to Accreditation Status...

Rules of Procedure for Approval of Law Schools Table of Contents I. Scope and Authority...49 Rule 1: Scope and Purpose... 49 Rule 2: Council Responsibility and Authority with Regard to Accreditation Status...

Syllabus for PRP 428 Public Relations Case Studies 3 Credit Hours Fall 2012

I. COURSE DESCRIPTION Syllabus for PRP 428 Public Relations Case Studies 3 Credit Hours Fall 2012 Models situations that organizations, managers, and public relations practitioners routinely face. Students

I. COURSE DESCRIPTION Syllabus for PRP 428 Public Relations Case Studies 3 Credit Hours Fall 2012 Models situations that organizations, managers, and public relations practitioners routinely face. Students

Guidelines for Mobilitas Pluss postdoctoral grant applications

Annex 1 APPROVED by the Management Board of the Estonian Research Council on 23 March 2016, Directive No. 1-1.4/16/63 Guidelines for Mobilitas Pluss postdoctoral grant applications 1. Scope The guidelines

Annex 1 APPROVED by the Management Board of the Estonian Research Council on 23 March 2016, Directive No. 1-1.4/16/63 Guidelines for Mobilitas Pluss postdoctoral grant applications 1. Scope The guidelines

REVIEW CYCLES: FACULTY AND LIBRARIANS** CANDIDATES HIRED ON OR AFTER JULY 14, 2014 SERVICE WHO REVIEWS WHEN CONTRACT

REVIEW CYCLES: FACULTY AND LIBRARIANS** CANDIDATES HIRED ON OR AFTER JULY 14, 2014 YEAR OF FOR WHAT SERVICE WHO REVIEWS WHEN CONTRACT FIRST DEPARTMENT SPRING 2 nd * DEAN SECOND DEPARTMENT FALL 3 rd & 4

REVIEW CYCLES: FACULTY AND LIBRARIANS** CANDIDATES HIRED ON OR AFTER JULY 14, 2014 YEAR OF FOR WHAT SERVICE WHO REVIEWS WHEN CONTRACT FIRST DEPARTMENT SPRING 2 nd * DEAN SECOND DEPARTMENT FALL 3 rd & 4

POLICIES AND PROCEDURES

UNIVERSITY OF HOUSTON - CLEAR LAKE School of Education POLICIES AND PROCEDURES December 10, 2004 Version 8.3 SCHOOL OF EDUCATION POLICIES AND PROCEDURES TABLE OF CONTENTS SECTION TITLE PAGE PREAMBLE...

UNIVERSITY OF HOUSTON - CLEAR LAKE School of Education POLICIES AND PROCEDURES December 10, 2004 Version 8.3 SCHOOL OF EDUCATION POLICIES AND PROCEDURES TABLE OF CONTENTS SECTION TITLE PAGE PREAMBLE...

COURSE INFORMATION. Course Number SER 216. Course Title Software Enterprise II: Testing and Quality. Credits 3. Prerequisites SER 215

**Disclaimer** This syllabus is to be used as a guideline only. The information provided is a summary of topics to be covered in the class. Information contained in this document such as assignments, grading

**Disclaimer** This syllabus is to be used as a guideline only. The information provided is a summary of topics to be covered in the class. Information contained in this document such as assignments, grading

STANISLAUS COUNTY CIVIL GRAND JURY CASE #08-04 LA GRANGE ELEMENTARY SCHOOL DISTRICT

STANISLAUS COUNTY CIVIL GRAND JURY 2007-2008 CASE #08-04 LA GRANGE ELEMENTARY SCHOOL DISTRICT SUMMARY A complaint was submitted to the Stanislaus County Grand Jury alleging that the La Grange Elementary

STANISLAUS COUNTY CIVIL GRAND JURY 2007-2008 CASE #08-04 LA GRANGE ELEMENTARY SCHOOL DISTRICT SUMMARY A complaint was submitted to the Stanislaus County Grand Jury alleging that the La Grange Elementary

Preferred method of written communication: elearning Message

Course ACCT 6356-501 Tax Research, Planning & Practice Professor Ronald J Blair, CPA, MBA Term Fall 2014 Meetings JSOM 2.803 Th 7 9:45 p.m. Professor's Contact Information Office Phone 972-883-4430 Office

Course ACCT 6356-501 Tax Research, Planning & Practice Professor Ronald J Blair, CPA, MBA Term Fall 2014 Meetings JSOM 2.803 Th 7 9:45 p.m. Professor's Contact Information Office Phone 972-883-4430 Office

Wolf Watch. A Degree Evaluation and Advising Tool. University of West Georgia

Wolf Watch A Degree Evaluation and Advising Tool University of West Georgia What is Wolf Watch? Software system that tracks degree progress, prepares for registration, and plans for graduation Web-based

Wolf Watch A Degree Evaluation and Advising Tool University of West Georgia What is Wolf Watch? Software system that tracks degree progress, prepares for registration, and plans for graduation Web-based

Charter School Reporting and Monitoring Activity

School Reporting and Monitoring Activity All information and documents listed below are to be provided to the Schools Office by the date shown, unless another date is specified in pre-opening conditions

School Reporting and Monitoring Activity All information and documents listed below are to be provided to the Schools Office by the date shown, unless another date is specified in pre-opening conditions

PLANNING FOR K TO 12. Don Brodeth, CFA Taft Consulting Group

PLANNING FOR K TO 12 Don Brodeth, CFA Taft Consulting Group donbrodeth@yahoo.com Our role as managers of schools. What are the challenges of K to12? How can my school plan for K to 12? A planning tool

PLANNING FOR K TO 12 Don Brodeth, CFA Taft Consulting Group donbrodeth@yahoo.com Our role as managers of schools. What are the challenges of K to12? How can my school plan for K to 12? A planning tool

REVIEW CYCLES: FACULTY AND LIBRARIANS** CANDIDATES HIRED PRIOR TO JULY 14, 2014 SERVICE WHO REVIEWS WHEN CONTRACT

REVIEW CYCLES: FACULTY AND LIBRARIANS** CANDIDATES HIRED PRIOR TO JULY 14, 2014 YEAR OF FOR WHAT SERVICE WHO REVIEWS WHEN CONTRACT FIFTH DEPARTMENT FALL 6 th & Tenure SENATE DEAN PROVOST, PRESIDENT NOTES:

REVIEW CYCLES: FACULTY AND LIBRARIANS** CANDIDATES HIRED PRIOR TO JULY 14, 2014 YEAR OF FOR WHAT SERVICE WHO REVIEWS WHEN CONTRACT FIFTH DEPARTMENT FALL 6 th & Tenure SENATE DEAN PROVOST, PRESIDENT NOTES:

b) Allegation means information in any form forwarded to a Dean relating to possible Misconduct in Scholarly Activity.

Allegation means information in any form forwarded to a Dean relating to possible Misconduct in Scholarly Activity.") University Policy University Procedure Instructions/Forms Integrity in Scholarly Activity Policy Classification Research Approval Authority General Faculties Council Implementation Authority Provost and

University Policy University Procedure Instructions/Forms Integrity in Scholarly Activity Policy Classification Research Approval Authority General Faculties Council Implementation Authority Provost and

UNA PROFESSIONAL ACCOUNTING PREP PROGRAM

UNA PROFESSIONAL ACCOUNTING PREP PROGRAM Course: AC 463P Financial Statement Auditing Professor: E-mail: Keith T. Jones, PhD, CPA Professor of Accounting University of North Alabama kjones5@una.edu TEXTBOOK:

UNA PROFESSIONAL ACCOUNTING PREP PROGRAM Course: AC 463P Financial Statement Auditing Professor: E-mail: Keith T. Jones, PhD, CPA Professor of Accounting University of North Alabama kjones5@una.edu TEXTBOOK:

Language Arts Methods

Language Arts Methods EDEE 424 Block 2 Fall 2015 Wednesdays, 2:00-3:20 pm On Campus, Laboratory Building E-132 & Online at Laulima.com Dr. Mary F. Heller Professor & Chair UHWO Division of Education mfheller@hawaii.edu

Language Arts Methods EDEE 424 Block 2 Fall 2015 Wednesdays, 2:00-3:20 pm On Campus, Laboratory Building E-132 & Online at Laulima.com Dr. Mary F. Heller Professor & Chair UHWO Division of Education mfheller@hawaii.edu

REQUEST FOR PROPOSALS SUPERINTENDENT SEARCH CONSULTANT

REQUEST FOR PROPOSALS SUPERINTENDENT SEARCH CONSULTANT Saint Paul Public Schools Independent School District # 625 360 Colborne Street Saint Paul MN 55102-3299 RFP Superintendent Search Consultant, St.

REQUEST FOR PROPOSALS SUPERINTENDENT SEARCH CONSULTANT Saint Paul Public Schools Independent School District # 625 360 Colborne Street Saint Paul MN 55102-3299 RFP Superintendent Search Consultant, St.

Charter School Performance Accountability

sept 2009 Charter School Performance Accountability The National Association of Charter School Authorizers (NACSA) is the trusted resource and innovative leader working with educators and public officials

sept 2009 Charter School Performance Accountability The National Association of Charter School Authorizers (NACSA) is the trusted resource and innovative leader working with educators and public officials

Conceptual Framework: Presentation

Meeting: Meeting Location: International Public Sector Accounting Standards Board New York, USA Meeting Date: December 3 6, 2012 Agenda Item 2B For: Approval Discussion Information Objective(s) of Agenda

Meeting: Meeting Location: International Public Sector Accounting Standards Board New York, USA Meeting Date: December 3 6, 2012 Agenda Item 2B For: Approval Discussion Information Objective(s) of Agenda

Navitas UK Holdings Ltd Embedded College Review for Educational Oversight by the Quality Assurance Agency for Higher Education

Navitas UK Holdings Ltd Embedded College Review for Educational Oversight by the Quality Assurance Agency for Higher Education February 2014 Annex: Birmingham City University International College Introduction

Navitas UK Holdings Ltd Embedded College Review for Educational Oversight by the Quality Assurance Agency for Higher Education February 2014 Annex: Birmingham City University International College Introduction

Accounting 380K.6 Accounting and Control in Nonprofit Organizations (#02705) Spring 2013 Professors Michael H. Granof and Gretchen Charrier

Spring 2013 Professors Michael H. Granof and Gretchen Charrier") Accounting 380K.6 Accounting and Control in Nonprofit Organizations (#02705) Spring 2013 Professors Michael H. Granof and Gretchen Charrier 1. Office: Prof Granof: CBA 4M.246; Prof Charrier: GSB 5.126D

Accounting 380K.6 Accounting and Control in Nonprofit Organizations (#02705) Spring 2013 Professors Michael H. Granof and Gretchen Charrier 1. Office: Prof Granof: CBA 4M.246; Prof Charrier: GSB 5.126D

CONFLICT OF INTEREST CALIFORNIA STATE UNIVERSITY, CHICO. Audit Report June 11, 2014

CONFLICT OF INTEREST CALIFORNIA STATE UNIVERSITY, CHICO Audit Report 14-19 June 11, 2014 Lupe C. Garcia, Chair Adam Day, Vice Chair Rebecca D. Eisen Steven M. Glazer Hugo N. Morales Members, Committee

CONFLICT OF INTEREST CALIFORNIA STATE UNIVERSITY, CHICO Audit Report 14-19 June 11, 2014 Lupe C. Garcia, Chair Adam Day, Vice Chair Rebecca D. Eisen Steven M. Glazer Hugo N. Morales Members, Committee

ACADEMIC AFFAIRS CALENDAR

ACADEMIC AFFAIRS CALENDAR 2017-2018 DUE DATE FALL 2017 TASKS RESPONSIBLE Friday, August 11 IELM Deadline for Deans to rank IELM cluster requests. Monday, August 14 Deadline for Faculty to Accept Temporary

ACADEMIC AFFAIRS CALENDAR 2017-2018 DUE DATE FALL 2017 TASKS RESPONSIBLE Friday, August 11 IELM Deadline for Deans to rank IELM cluster requests. Monday, August 14 Deadline for Faculty to Accept Temporary

ASCD Recommendations for the Reauthorization of No Child Left Behind

ASCD Recommendations for the Reauthorization of No Child Left Behind The Association for Supervision and Curriculum Development (ASCD) represents 178,000 educators. Our membership is composed of teachers,

ASCD Recommendations for the Reauthorization of No Child Left Behind The Association for Supervision and Curriculum Development (ASCD) represents 178,000 educators. Our membership is composed of teachers,

BSP !!! Trainer s Manual. Sheldon Loman, Ph.D. Portland State University. M. Kathleen Strickland-Cohen, Ph.D. University of Oregon

Basic FBA to BSP Trainer s Manual Sheldon Loman, Ph.D. Portland State University M. Kathleen Strickland-Cohen, Ph.D. University of Oregon Chris Borgmeier, Ph.D. Portland State University Robert Horner,

Basic FBA to BSP Trainer s Manual Sheldon Loman, Ph.D. Portland State University M. Kathleen Strickland-Cohen, Ph.D. University of Oregon Chris Borgmeier, Ph.D. Portland State University Robert Horner,

University of Toronto

University of Toronto OFFICE OF THE VICE PRESIDENT AND PROVOST Framework for the Divisional Appeals Processes The purpose of the Framework is to provide guidance and advice for the establishment of appropriate

University of Toronto OFFICE OF THE VICE PRESIDENT AND PROVOST Framework for the Divisional Appeals Processes The purpose of the Framework is to provide guidance and advice for the establishment of appropriate

Book Reviews. Michael K. Shaub, Editor

ISSUES IN ACCOUNTING EDUCATION Vol. 26, No. 3 2011 pp. 633 637 American Accounting Association DOI: 10.2308/iace-10118 Book Reviews Michael K. Shaub, Editor Editor s Note: Books for review should be sent

ISSUES IN ACCOUNTING EDUCATION Vol. 26, No. 3 2011 pp. 633 637 American Accounting Association DOI: 10.2308/iace-10118 Book Reviews Michael K. Shaub, Editor Editor s Note: Books for review should be sent

Youth Sector 5-YEAR ACTION PLAN ᒫᒨ ᒣᔅᑲᓈᐦᒉᑖ ᐤ. Office of the Deputy Director General

Youth Sector 5-YEAR ACTION PLAN ᒫᒨ ᒣᔅᑲᓈᐦᒉᑖ ᐤ Office of the Deputy Director General Produced by the Pedagogical Management Team Joe MacNeil, Ida Gilpin, Kim Quinn with the assisstance of John Weideman and

Youth Sector 5-YEAR ACTION PLAN ᒫᒨ ᒣᔅᑲᓈᐦᒉᑖ ᐤ Office of the Deputy Director General Produced by the Pedagogical Management Team Joe MacNeil, Ida Gilpin, Kim Quinn with the assisstance of John Weideman and

MASTER OF ARTS IN APPLIED SOCIOLOGY. Thesis Option

MASTER OF ARTS IN APPLIED SOCIOLOGY Thesis Option As part of your degree requirements, you will need to complete either an internship or a thesis. In selecting an option, you should evaluate your career

MASTER OF ARTS IN APPLIED SOCIOLOGY Thesis Option As part of your degree requirements, you will need to complete either an internship or a thesis. In selecting an option, you should evaluate your career

Developing Regional Work-Based Learning

Developing Regional Work-Based Learning Systems @NAFCareerAcads z Presenters Alliance for Linked Learning, Oxnard CA: Jim Rose, Director, Career Pathways and Community Partnerships East Bay Career Pathways:

Developing Regional Work-Based Learning Systems @NAFCareerAcads z Presenters Alliance for Linked Learning, Oxnard CA: Jim Rose, Director, Career Pathways and Community Partnerships East Bay Career Pathways:

Guidelines for Mobilitas Pluss top researcher grant applications

Annex 1 APPROVED by the Management Board of the Estonian Research Council on 23 March 2016, Directive No. 1-1.4/16/63 Guidelines for Mobilitas Pluss top researcher grant applications 1. Scope The guidelines

Annex 1 APPROVED by the Management Board of the Estonian Research Council on 23 March 2016, Directive No. 1-1.4/16/63 Guidelines for Mobilitas Pluss top researcher grant applications 1. Scope The guidelines

TEXAS CHRISTIAN UNIVERSITY M. J. NEELEY SCHOOL OF BUSINESS CRITERIA FOR PROMOTION & TENURE AND FACULTY EVALUATION GUIDELINES 9/16/85*

TEXAS CHRISTIAN UNIVERSITY M. J. NEELEY SCHOOL OF BUSINESS CRITERIA FOR PROMOTION & TENURE AND FACULTY EVALUATION GUIDELINES 9/16/85* Effective Fall of 1985 Latest Revision: April 9, 2004 I. PURPOSE AND

TEXAS CHRISTIAN UNIVERSITY M. J. NEELEY SCHOOL OF BUSINESS CRITERIA FOR PROMOTION & TENURE AND FACULTY EVALUATION GUIDELINES 9/16/85* Effective Fall of 1985 Latest Revision: April 9, 2004 I. PURPOSE AND

Information Sheet for Home Educators in Tasmania

HOME EDUCATION ASSOCIATION, Inc. PO Box 245 Petersham NSW 2049 1300 72 99 91 www.hea.edu.au admin@hea.edu.au Information Sheet for Home Educators in Tasmania How the Draft Tasmanian Education Bill 2016

HOME EDUCATION ASSOCIATION, Inc. PO Box 245 Petersham NSW 2049 1300 72 99 91 www.hea.edu.au admin@hea.edu.au Information Sheet for Home Educators in Tasmania How the Draft Tasmanian Education Bill 2016

Synchronous Blended Learning Best Practices

Synchronous Blended Learning Best Practices Andrew Shields, Manager of Technology-based Learning, May 18 19, 2006 Produced by 202 Synchronous Blended Learning Best Practices Presented By Andrew Shields

Synchronous Blended Learning Best Practices Andrew Shields, Manager of Technology-based Learning, May 18 19, 2006 Produced by 202 Synchronous Blended Learning Best Practices Presented By Andrew Shields

Department of Legal Assistant Education THE SOONER DOCKET. Enroll Now for Spring 2018 Courses! American Bar Association Approved

Department of Legal Assistant Education THE SOONER DOCKET Enroll Now for Spring 2018 Courses! American Bar Association Approved Vol. 40, No. 2 November 2017 Legal Assistant Education Schedule SPRING 2018

Department of Legal Assistant Education THE SOONER DOCKET Enroll Now for Spring 2018 Courses! American Bar Association Approved Vol. 40, No. 2 November 2017 Legal Assistant Education Schedule SPRING 2018

TSI Operational Plan for Serving Lower Skilled Learners

TSI Operational Plan for Serving Lower Skilled Learners VERSION 2.0* *This document represents a work in progress that is informed by and revised based on stakeholder comments and feedback. Each revised

TSI Operational Plan for Serving Lower Skilled Learners VERSION 2.0* *This document represents a work in progress that is informed by and revised based on stakeholder comments and feedback. Each revised

Personal Project. IB Guide: Project Aims and Objectives 2 Project Components... 3 Assessment Criteria.. 4 External Moderation.. 5

Table of Contents: Personal Project IB Guide: Project Aims and Objectives 2 Project Components..... 3 Assessment Criteria.. 4 External Moderation.. 5 General Guidelines: Process Journal. 5 Product 7 Personal

Table of Contents: Personal Project IB Guide: Project Aims and Objectives 2 Project Components..... 3 Assessment Criteria.. 4 External Moderation.. 5 General Guidelines: Process Journal. 5 Product 7 Personal

The FPA Diversity Scholarship Program is available for the following FPA National Conferences:

Guidelines Overview The primary aim of the Financial Planning Association (FPA ) is to be the community that fosters the value of financial planning and advances the financial planning profession. FPA

Guidelines Overview The primary aim of the Financial Planning Association (FPA ) is to be the community that fosters the value of financial planning and advances the financial planning profession. FPA

MSE 5301, Interagency Disaster Management Course Syllabus. Course Description. Prerequisites. Course Textbook. Course Learning Objectives

MSE 5301, Interagency Disaster Management Course Syllabus Course Description Focuses on interagency cooperation for complex crises and domestic emergencies. Reviews the coordinating mechanisms and planning

MSE 5301, Interagency Disaster Management Course Syllabus Course Description Focuses on interagency cooperation for complex crises and domestic emergencies. Reviews the coordinating mechanisms and planning

Intermediate Algebra

Intermediate Algebra An Individualized Approach Robert D. Hackworth Robert H. Alwin Parent s Manual 1 2005 H&H Publishing Company, Inc. 1231 Kapp Drive Clearwater, FL 33765 (727) 442-7760 (800) 366-4079

Intermediate Algebra An Individualized Approach Robert D. Hackworth Robert H. Alwin Parent s Manual 1 2005 H&H Publishing Company, Inc. 1231 Kapp Drive Clearwater, FL 33765 (727) 442-7760 (800) 366-4079

MADISON METROPOLITAN SCHOOL DISTRICT

MADISON METROPOLITAN SCHOOL DISTRICT Section 504 Manual for Identifying and Serving Eligible Students: Guidelines, Procedures and Forms TABLE OF CONTENTS INTRODUCTION. 1 OVERVIEW.. 2 POLICY STATEMENT 3

MADISON METROPOLITAN SCHOOL DISTRICT Section 504 Manual for Identifying and Serving Eligible Students: Guidelines, Procedures and Forms TABLE OF CONTENTS INTRODUCTION. 1 OVERVIEW.. 2 POLICY STATEMENT 3

WE GAVE A LAWYER BASIC MATH SKILLS, AND YOU WON T BELIEVE WHAT HAPPENED NEXT

WE GAVE A LAWYER BASIC MATH SKILLS, AND YOU WON T BELIEVE WHAT HAPPENED NEXT PRACTICAL APPLICATIONS OF RANDOM SAMPLING IN ediscovery By Matthew Verga, J.D. INTRODUCTION Anyone who spends ample time working

WE GAVE A LAWYER BASIC MATH SKILLS, AND YOU WON T BELIEVE WHAT HAPPENED NEXT PRACTICAL APPLICATIONS OF RANDOM SAMPLING IN ediscovery By Matthew Verga, J.D. INTRODUCTION Anyone who spends ample time working

Exercise Format Benefits Drawbacks Desk check, audit or update

Guidance Note 6 Exercising for Resilience With critical activities, resources and recovery priorities established, and preparations made for crisis management, all preparations and plans should be tested

Guidance Note 6 Exercising for Resilience With critical activities, resources and recovery priorities established, and preparations made for crisis management, all preparations and plans should be tested

ARKANSAS TECH UNIVERSITY

ARKANSAS TECH UNIVERSITY Procurement and Risk Management Services Young Building 203 West O Street Russellville, AR 72801 REQUEST FOR PROPOSAL Search Firms RFP#16-017 Due February 26, 2016 2:00 p.m. Issuing

ARKANSAS TECH UNIVERSITY Procurement and Risk Management Services Young Building 203 West O Street Russellville, AR 72801 REQUEST FOR PROPOSAL Search Firms RFP#16-017 Due February 26, 2016 2:00 p.m. Issuing

Jon N. Kerr, PhD, CPA August 2017

JON NATHAN KERR, PhD, CPA ASSISTANT PROFESSOR THE OHIO STATE UNIVERSITY FISHER COLLEGE OF BUSINESS 2100 NEIL AVENUE 400 FISHER HALL COLUMBUS, OH 43210 Email: kerr.360@osu.edu Office: Fax: EDUCATION Columbia

JON NATHAN KERR, PhD, CPA ASSISTANT PROFESSOR THE OHIO STATE UNIVERSITY FISHER COLLEGE OF BUSINESS 2100 NEIL AVENUE 400 FISHER HALL COLUMBUS, OH 43210 Email: kerr.360@osu.edu Office: Fax: EDUCATION Columbia

Welcome to The National Training Institute for Child Care Health Consultants

Welcome to The National Training Institute for Child Care Health Consultants. 1 Introductions/Icebreaker: Acknowledging Trainers Expertise Front of Card First and last name State Back of Card Agency #

Welcome to The National Training Institute for Child Care Health Consultants. 1 Introductions/Icebreaker: Acknowledging Trainers Expertise Front of Card First and last name State Back of Card Agency #

Oklahoma State University Policy and Procedures

Oklahoma State University Policy and Procedures REAPPOINTMENT, PROMOTION AND TENURE PROCESS FOR RANKED FACULTY 2-0902 ACADEMIC AFFAIRS September 2015 PURPOSE The purpose of this policy and procedures letter

Oklahoma State University Policy and Procedures REAPPOINTMENT, PROMOTION AND TENURE PROCESS FOR RANKED FACULTY 2-0902 ACADEMIC AFFAIRS September 2015 PURPOSE The purpose of this policy and procedures letter

Standards and Criteria for Demonstrating Excellence in BACCALAUREATE/GRADUATE DEGREE PROGRAMS

Standards and Criteria for Demonstrating Excellence in BACCALAUREATE/GRADUATE DEGREE PROGRAMS World Headquarters 11520 West 119th Street Overland Park, KS 66213 USA USA Belgium Perú acbsp.org info@acbsp.org

Standards and Criteria for Demonstrating Excellence in BACCALAUREATE/GRADUATE DEGREE PROGRAMS World Headquarters 11520 West 119th Street Overland Park, KS 66213 USA USA Belgium Perú acbsp.org info@acbsp.org

Guidance on the University Health and Safety Management System

Newcastle University Safety Office 1 Kensington Terrace Newcastle upon Tyne NE1 7RU Tel 0191 222 6274 University Safety Policy Guidance Guidance on the University Health and Safety Management System Document

Newcastle University Safety Office 1 Kensington Terrace Newcastle upon Tyne NE1 7RU Tel 0191 222 6274 University Safety Policy Guidance Guidance on the University Health and Safety Management System Document

The completed proposal should be forwarded to the Chief Instructional Officer and the Academic Senate.

Academic Department Proposal Template The purpose of this template is to assist faculty and others in preparing the proposals required by AP 4023 (Academic Departments) for Initiation, Merging, Splitting

Academic Department Proposal Template The purpose of this template is to assist faculty and others in preparing the proposals required by AP 4023 (Academic Departments) for Initiation, Merging, Splitting

CONNECTICUT GUIDELINES FOR EDUCATOR EVALUATION. Connecticut State Department of Education

CONNECTICUT GUIDELINES FOR EDUCATOR EVALUATION Connecticut State Department of Education October 2017 Preface Connecticut s educators are committed to ensuring that students develop the skills and acquire

CONNECTICUT GUIDELINES FOR EDUCATOR EVALUATION Connecticut State Department of Education October 2017 Preface Connecticut s educators are committed to ensuring that students develop the skills and acquire

Sacramento State Degree Revocation Policy and Procedure

Sacramento State Degree Revocation Policy and Procedure California State University Sacramento s 1 award of academic credit and Degrees constitutes its certification of student achievement. However, a

Sacramento State Degree Revocation Policy and Procedure California State University Sacramento s 1 award of academic credit and Degrees constitutes its certification of student achievement. However, a

USC VITERBI SCHOOL OF ENGINEERING

USC VITERBI SCHOOL OF ENGINEERING APPOINTMENTS, PROMOTIONS AND TENURE (APT) GUIDELINES Office of the Dean USC Viterbi School of Engineering OHE 200- MC 1450 Revised 2016 PREFACE This document serves as

USC VITERBI SCHOOL OF ENGINEERING APPOINTMENTS, PROMOTIONS AND TENURE (APT) GUIDELINES Office of the Dean USC Viterbi School of Engineering OHE 200- MC 1450 Revised 2016 PREFACE This document serves as

Upward Bound Program

SACS Preparation Division of Student Affairs Upward Bound Program REQUIREMENTS: The institution provides student support programs, services, and activities consistent with its mission that promote student

SACS Preparation Division of Student Affairs Upward Bound Program REQUIREMENTS: The institution provides student support programs, services, and activities consistent with its mission that promote student

Comments to PCAOB Rulemaking Docket Matter No. 37 "CONCEPT RELEASE ON AUDITOR INDEPENDENCE AND AUDIT FIRM ROTATION"

Comments to PCAOB Rulemaking Docket Matter No. 37 "CONCEPT RELEASE ON AUDITOR INDEPENDENCE AND AUDIT FIRM ROTATION" Even if the academic literature has studied the effects of the introduction of the mandatory

Comments to PCAOB Rulemaking Docket Matter No. 37 "CONCEPT RELEASE ON AUDITOR INDEPENDENCE AND AUDIT FIRM ROTATION" Even if the academic literature has studied the effects of the introduction of the mandatory

Audit and Compliance Committee - Agenda

Audit and Compliance Committee - Agenda Board of Trustees Audit and Compliance Committee August 11, 2017, 9:00-10:00 am President s Board Room Conference Call-In Phone #1-800-442-5794, passcode 463796

Audit and Compliance Committee - Agenda Board of Trustees Audit and Compliance Committee August 11, 2017, 9:00-10:00 am President s Board Room Conference Call-In Phone #1-800-442-5794, passcode 463796

Higher Education Review (Embedded Colleges) of Navitas UK Holdings Ltd. Hertfordshire International College

of Navitas UK Holdings Ltd. Hertfordshire International College") Higher Education Review (Embedded Colleges) of Navitas UK Holdings Ltd April 2016 Contents About this review... 1 Key findings... 2 QAA's judgements about... 2 Good practice... 2 Theme: Digital Literacies...

Higher Education Review (Embedded Colleges) of Navitas UK Holdings Ltd April 2016 Contents About this review... 1 Key findings... 2 QAA's judgements about... 2 Good practice... 2 Theme: Digital Literacies...

BACKGROUND NOTE ON ACTION PLANS

BACKGROUND NOTE ON ACTION PLANS Action Plans are developed by IFAC members and associates to address policy matters identified through their responses to the IFAC Compliance Self-Assessment Questionnaire.

BACKGROUND NOTE ON ACTION PLANS Action Plans are developed by IFAC members and associates to address policy matters identified through their responses to the IFAC Compliance Self-Assessment Questionnaire.

THE QUEEN S SCHOOL Whole School Pay Policy

The Queen s Church of England Primary School Encouraging every child to reach their full potential, nurtured and supported in a Christian community which lives by the values of Love, Compassion and Respect.

The Queen s Church of England Primary School Encouraging every child to reach their full potential, nurtured and supported in a Christian community which lives by the values of Love, Compassion and Respect.

BEST PRACTICES FOR PRINCIPAL SELECTION

BEST PRACTICES FOR PRINCIPAL SELECTION This document guides councils through legal requirements and suggested best practices of the principal selection process. These suggested steps are written with the

BEST PRACTICES FOR PRINCIPAL SELECTION This document guides councils through legal requirements and suggested best practices of the principal selection process. These suggested steps are written with the