A primer on the types of higher education tax benefits available to families.

|

|

|

- Irene Washington

- 6 years ago

- Views:

Transcription

1 A primer on the types of higher education tax benefits available to families. The federal government provides financial assistance for higher education in four broad categories grants, work study, loans and tax benefits. For the majority of the last fifty years and ever since the federal government first began providing financial assistance for higher education in the 1950s, the dominant forms of aid have been grants, work study assistance, and loans. SOURCE: TRENDS IN STUDENT AID 2016 Since the mid-1990s, however, federal income tax benefits have increasingly become a part of the student financial aid landscape. Over the last decade, federal expenditures (foregone tax revenue) in the form of higher education tax benefits have increased 109 percent. In , federal education tax benefits made up seven percent of total student aid (federal, state,

2 institutional, private, including loans) for postsecondary education. Looking only at federal student aid in that year, education tax benefits constituted $18.3 billion, or 11.5 percent, of the $158.3 billion in financial assistance, including loans. Student Aid for Higher Education in 2015 Dollars (numbers in millions) Year % Change Pell Grants $15,503 $39,055 $28,232 82% Other Federal Grants (Including Veterans and Military) $5,531 $14,113 $15, % Federal Loans $70,626 $116,256 $95,826 36% Federal Work-Study $1,202 $1,067 $982-18% Federal Tax Benefits $7,814 $21,689 $18, % State Grants $8,602 $10,117 $10,526 22% Institutional Grants $29,082 $41,954 $54,705 88% Private and Employer Grants $11,517 $14,548 $17,426 51% Source: Trends in Student Aid 2016 The number of students and families receiving tax benefits for postsecondary education was 13.8 million in , making this category of federal financial aid assistance the most utilized of all federal financial aid programs. Though they are the most used form of federal financial aid (with the exception of the Supplemental Educational Opportunity Grant), federal education tax benefits represent the smallest average amount of aid per individual with an average benefit of $1,320.

3 Recipients of Federal Student Aid in Millions (with Average Aid Per Recipient) Education Tax Benefits ($1,320) Pell Grants ($3,720) Unsubsidized Loans ($6,980) Subsidized Loans ($3,800) Supplemental Educational Opt. Grant ($450) Veteran's Post-9/11 GI Education Benefits ($14,570) Work-Study ($1,550) Perkins Loans ($2,400) SOURCE: TRENDS IN STUDENT AID 2016 Types of Federal Higher Education Benefits Generally speaking, the Internal Revenue Code provides four categories of tax benefits credits, deductions, exemptions and exclusions. These benefits may either reduce an individual s tax liability (i.e., the amount of taxes an individual owes) or reduce the amount of an individual s income that is subject to taxation. Tax Credit: Tax credits reduce the amount of tax a tax filer owes on a dollar-for-dollar basis. A tax credit may be either nonrefundable or refundable. A nonrefundable credit can only reduce a tax filer s tax bill to $0 and cannot produce a tax refund where one did not already exist. A refundable tax credit, on the other hand, can exceed taxes owed and can result in a tax refund. Tax Deduction: Tax deductions reduce the amount of a tax filer s income that is subject to taxation. The eligible tax deduction amount is the amount of reduction to a taxpayer s taxable income. Thus, if an individual is eligible for a $2,000 tax deduction and his or her

4 taxable income is $50,000 prior to taking the deduction, the individual s taxable income after taking the deduction would be $48,000. Tax Exemption: Tax exemptions work in the same way as do tax deductions in reducing an individual s taxable income. The most common tax exemptions are the personal and dependent exemptions. Tax filers may claim a personal exemption for themselves and any dependents they support. The personal exemption for tax year 2016 is $4,050. Tax Exclusion: The Internal Revenue Code contains a number of provisions that explicitly exclude certain types of income or amounts of income from taxation. These types of income are not included as taxable income. Over the years, Congress has enacted a number of tax benefits specifically to assist individuals and families in paying for college. These higher education tax benefits come in all types credits, deductions, exemptions, and exclusions and may broadly be divided into four categories: tax benefits for tuition and related expenses, employment-related higher education tax benefits, tax benefits for student loans, and tax benefits for education savings. Many of these higher education tax benefits have been part of the Internal Revenue Code for several decades and some date back to the 1950s. Yet, prior to enactment of the Taxpayer Relief Act of 1997 (P.L ), tax benefits for higher education remained a relatively small part of the federal financial aid picture. Prior to the Taxpayer Relief Act of 1997, Congress enacted the following tax benefits for higher education: Personal Exemption for Dependents Ages Qualified Scholarship Exclusion

5 Gift Tax Exclusion for Education Employer-Provided Educational Assistance Employer-Provided Qualified Tuition Reduction Business Deduction for Education-Related Expenses Student Loan Interest Deduction Exclusion of Qualifying Cancelled Student Loans 529 Plans Exclusion of Interest on Education Savings Bonds When President Clinton announced his Administration s proposal for providing middle class families with tax credits to pay for college in 1996, the idea of using the Internal Revenue Code as a piece of the student financial aid puzzle firmly took hold. Middle class families who felt they were being priced out of college, but who did not qualify for Pell or subsidized loans, finally felt as if they were getting a break they deserved. Signed into law in 1997, the Taxpayer Relief Act of 1997 (P.L ) created four additional higher education tax benefits and reinstated the student loan interest deduction which had been eliminated from the tax code as part of the Tax Reform Act of 1986 (P.L ). The tax benefits in the 1997 Taxpayer Relief Act were: Hope Scholarship Credit Lifetime Learning Credit Student Loan Interest Deduction Coverdell Education Savings Accounts Cancellations of the Penalty for Early Withdrawals from Individual Retirement Accounts (IRAs) In 2001, as part of the Economic Growth and Tax Relief Act of 2001 (P.L ), Congress added two new tax benefits the tuition and fees deduction and tax-free distributions from 529 college savings plans. Then, as part of the American Recovery and Reinvestment Act of 2009 (P.L ), Congress temporarily replaced the Hope Scholarship Credit with the more generous American Opportunity Tax Credit. In 2015, lawmakers made the REPLACMENT permanent under the Protecting Americans from Tax Hikes (PATH) Act of 2015 (P.L ). Most of these tax benefits have provisions that disallow tax filers from using the same qualified educational expense to claim more than one tax benefit. Because many tax filers may meet the qualifications for more than one tax benefit, individuals must examine each benefit separately to determine which offers the greatest financial benefit. Current Considerations and Issues

, and the introduction of higher education tax credits, the popularity of using the Internal Revenue Code as a means of offering students and families, especially middle class families,")

6 Since enactment of the Taxpayer Relief Act of 1997 (P.L ), and the introduction of higher education tax credits, the popularity of using the Internal Revenue Code as a means of offering students and families, especially middle class families, financial aid to pay for college has grown. While popular, a number of reports have indicated that the sheer number of benefits and complex eligibility rules often make it difficult for families to understand the tax benefits for which they may be eligible and choose the tax benefit that is most financially beneficial to them. A 2012 report issued by the Government Accountability Office (GAO) found that in tax year 2009 almost 14 percent of filers failed to claim a higher education credit or deduction for which they were eligible. i That same GAO report lays out a number of possible reasons for families either failing to claim a benefit for which they are eligible or for making a suboptimal choice (i.e., choosing a less financially beneficial option) in their selection of education tax benefits. These reasons include lack of awareness or misunderstanding of eligibility, confusion over the sheer number of provisions, similarity in provisions making it difficult to determine which one may be best, and differences in key definitions such as the multiple definitions for qualified education expenses. A 2015 report by New America also found that about 40 percent of undergraduate students are ineligible for any federal tuition tax benefit because they do not pay tuition or do not file taxes. Most of those families (63.5 percent) do not have any tuition or fee expenses net of other grants and scholarships and therefore have no expenses to offset. About 31 percent of those ineligible for a benefit did not file federal income taxes, making them ineligible. There is some overlap between these two groups. Many of these students attend community colleges, and a majority of them earn less than $30,000 per year. ii SOURCE: NEW AMERICA

7 Growth in the uptake of these tax credits and deductions was relatively flat for much of the 2000s, but their popularity and uptake have more than doubled in recent years. This uptick was caused almost exclusively by the introduction of the more generous American Opportunity Tax Credit in In 2014, 13.8 million tax filers benefited from a federal tuition tax credit or deduction for a total of $18.2 billion in tax savings. $25 Total Education Tax Credits and Savings from Tuition Deductions in Billions of 2014 Dollars $20 $15 $10 $5 $ SOURCE: TRENDS IN STUDENT AID 2016 At a time of budget constraints, some have questioned whether spending on tax benefits might better be directed towards traditional financial aid programs Pell, loans, work study, etc., especially those traditional programs that are more targeted to lower-income families and students. In 2014, 53 percent of higher education tax benefits went to families with adjusted gross incomes above $50,000, with 24 percent going to families with adjusted gross incomes above $100,000. Additionally, for both the credits and the deduction, the average tax savings per recipient is greater for both middle and upper-income families. Analysis by New America provides yet another perspective for policymakers regarding the targeting of tuition tax benefits. The breakdown of tax benefit eligibility by institution type (i.e. four-year public, community college, etc.) reveals that students attending more expensive private and non-profit and for-profit schools are over represented among undergraduates eligible for tax benefits. Students attending lower cost public four-year and community colleges are underrepresented. Students at lower cost schools incur lower out-of-pocket costs after grant aid is factored in and therefore have few costs with which to claim a tuition tax benefit. iii

8 Distribution of Education Tax Credits and Savings from Tuition Deduction by Adjusted Gross Income (AGI), 2014 $100,000 to $180,000 $75,000 to $99,999 $50,000 to $74,999 $25,000 to $49,999 Less than $25,000 0% 5% 10% 15% 20% 25% 30% SOURCE: TRENDS IN STUDENT AID 2016 A final set of considerations related to higher education tax benefits concerns their effectiveness in meeting public policy goals. A GAO report in response to Congressional inquiries on the effectiveness of both Title IV and federal higher education tax benefits found that research into the effects of these programs on college attendance, choice, cost, persistence, and completion is scant and questions of effectiveness remain largely unanswered. iv As Congress takes up comprehensive tax reform and the re-authorization of the Higher Education Act for consideration, questions related to the purposes, target populations, and effectiveness of all forms of federal financial assistance for higher education education tax benefits and traditional Title IV aid may be in order. Details of Federal Higher Education Tax Benefits American Opportunity Tax Credit (IRC Sec. 25A) The American Opportunity Tax Credit (AOTC) is for undergraduate education. As mentioned earlier, the AOTC is a more generous version of the original Hope Scholarship Credit that it replaced. In addition to the AOTC providing a higher maximum benefit than Hope, the AOTC covers four years of college as opposed to two, has higher income phase-out limits, and has a broader definition of qualified education expenses. The AOTC is also a partially refundable credit. Thus, under the non-refundable Hope, if a tax filer has $0 tax liability, the tax filer receives no financial benefit. However, under AOTC, which is partially refundable, a tax filer with $0 tax liability may still receive a financial benefit of up to $1,000, provided he has

9 incurred that much in tuition expenses. Many students and families who have no federal tax liability qualify for enough grant aid that they do not pay any tuition expenses. Details of the features of the American Opportunity Tax Credit follow.

Unlike the American Opportunity Tax Credit and the Hope Credit which are both for undergraduate education exclusively, the Lifetime Learning Credit may be used at any postsecondary education")

10 Lifetime Leaning Credit (IRC Sec. 25A) Unlike the American Opportunity Tax Credit and the Hope Credit which are both for undergraduate education exclusively, the Lifetime Learning Credit may be used at any postsecondary education level undergraduate or graduate. Additionally, while a student must be enrolled on at least a half-time basis and in a program leading to a degree or credential to qualify for the AOTC or Hope, to claim the Lifetime Learning Credit a student need only enroll in one or more classes that may or may not lead to a degree or credential.

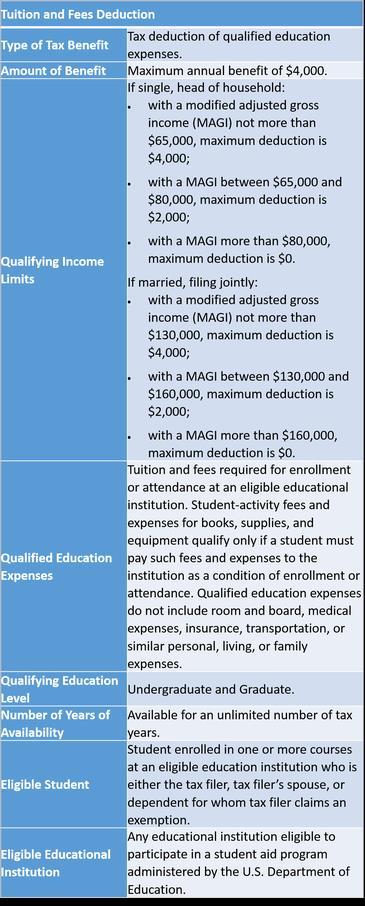

11 Tuition and Fees Deduction (IRC Sec. 222) In 2001, Congress created a third tax benefit to assist families and students cover the cost of college. Similar to the Lifetime Learning Credit, the Tuition and Fees deduction covers both undergraduate and graduate education and may be used for one or more classes. Congress has typically only enacted the deduction on a temporary basis. In fact, the deduction was extended in time for the 2015 tax filing season. In addition to being a deduction rather than a credit, the deduction also has higher income limits than the Lifetime credit (but not the American Opportunity Tax Credit). While the Lifetime credit phases out between $55,000 and $65,000 (single) / $110,000 and $130,000 (joint), the income limits for the Tuition and Fees Deduction were $80,000 for single filers and $160,000 for joint filers. However, the American Opportunity Tax Credit now has the highest income limits of the tax benefits for tuition, phasing out at $90,000 (single) / $180,000 (joint). In recent years, the number of tax filers claiming the Tuition and Fees Deduction has dropped off considerably, falling from 4.6 million in 2008 to 1.7 million in This is due in large part to creation of the American Opportunity Tax Credit, which is partially refundable and which has even higher income limit phase outs than the Tuition and Fees Deduction. Filers claiming the Tuition and Fees deduction are likely graduate students or undergraduates enrolled beyond a fourth year, two groups who are ineligible for the American Opportunity Tax Credit.

12

13 Exclusion for Qualified Scholarships (IRC Sec. 117) One of the oldest tax benefits for higher education is the exclusion for qualified scholarships. Since 1954, tax filers have been able to exclude from their income all or part of the funds they receive through a scholarship. Up until the 1986 tax reform bill (P.L ), students could exclude scholarship funds for tuition and many other college expenses from their income. Today, however, students may only exclude those scholarship funds used to cover expenses directly related to education, e.g., tuition, fees, books. Scholarship funds used to cover room and board and other expenses are subject to taxation. Personal Exemption for Dependents Ages (IRC Sec. 151 & 152) While typically a parent cannot claim a child over the age of 18 as a dependent for federal income tax purposes, if a child is ages and is enrolled full time for at least five months of the year at a school with a regular teaching staff, course of study, and a regularly enrolled student body, a parent may claim a personal exemption for the child. For tax year 2016, a parent may receive a tax benefit of $4,050 for each qualifying dependent. For tax year 2013 and beyond, a personal exemption phase-out applies. The phase-out level for single tax filers begins at $259,400, and $311,300 for married couples filing jointly. Gift Tax Exclusions for Higher Education Expenses (IRC Sec. 2503(b) and 2503(e)) Under current federal tax law, two gift tax exclusions exist that may be used to cover higher education expenses. First, under IRC Sec. 2503(b), a donor may give any individual up to $14,000 a year (tax year 2016 limit) for higher education expenses without incurring the federal gift tax. Second, in addition to the general annual gift tax exclusion, a donor may make a direct payment for tuition (no limit) to an institution of higher education on behalf of an individual without incurring the federal gift tax (IRC Sec. 2503(e)). This second gift tax exclusion is for tuition only and does not include payments for books, supplies, or room and board. There are no income restrictions on these gift tax exclusions. Student Loan Interest Deduction (IRC Sec. 221) The ability to take a federal deduction for interest paid on student loan debt is one of the oldest federal higher education tax benefits and one that has been allowed and disallowed at various points in time. Prior to 1986, student loan interest, like other types of personal debt (e.g., mortgage, credit card, auto), was deductible under the federal tax code. The 1986 comprehensive tax reform law (P.L ) disallowed deductions for all forms of personal debt interest other than mortgage interest, including student loan interest. The ability to deduct student loan interest remained out of the tax code for the next ten years until passage of the Taxpayer Relief Act of 1997 (P.L ). This law restored the deduction; however, students were only able to take the deduction for the first five years of repayment. The Economic Growth and Tax Relief Reconciliation Act of 2001 (P.L ) temporarily lifted the five-year rule, and American Taxpayer Relief Act of 2012 (P.L ) permanently lifted the limit. Today, if student borrowers meet the other eligibility requirements, they may take the deduction for as many years as they pay interest on their student loans, federal or private. In tax year 2014, 12.1 million tax filers deducted $12.8 billion in student loan interest. v

) Generally, any portion of a student loan that is cancelled or forgiven must be included in gross income and therefore be subject to tax.")

14 Tax-Free Treatment of Student Loan Cancellations and Student Loan Repayment Assistance (IRC Sec. 108(f)) Generally, any portion of a student loan that is cancelled or forgiven must be included in gross income and therefore be subject to tax. However, in certain circumstances federal tax law excludes such loan forgiveness as taxable income. To qualify for tax-free treatment the loan must have been made by a qualified lender and require that the student work for a certain period of time, in a certain profession, and for any of a broad class of employers. Two of the best known examples of student loan cancellations qualifying for tax-free treatment are the Public Service Loan Forgiveness and Teacher Loan Forgiveness programs authorized under Title IV of the Higher Education Act.

15 Additionally, payments that students receive from their participation in certain health service loan repayment programs are also tax-free. These programs are: The National Health Service Corps Loan Repayment Program. A state education loan repayment program eligible for funds under the Public Health Service Act. Any other state loan repayment or loan forgiveness program intended to increase the availability of health services in underserved or health shortage areas. Over the years, Congress has added education-related provisions to the tax code to assist employers in attracting and retaining talented employees and to assist employees in continuing their education and obtaining new knowledge and skills. Three of these employment-related provisions are the Employer-Provided Educational Assistance provision, the Employer-Provided Qualified Tuition Plan, and the Business Deduction for Education-Related Expenses.

Under section 127 of the Internal Revenue Code, up to $5,250 received in employer-provided educational assistance may be excluded from an employee s gross income.")

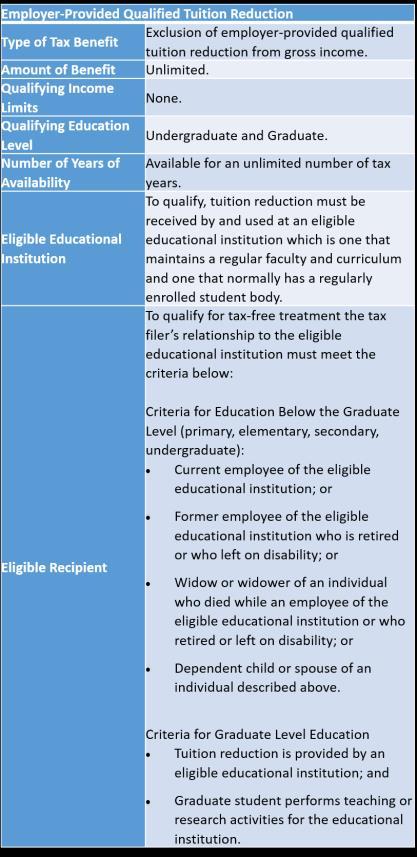

16 Employer-Provided Educational Assistance (IRC Sec. 127) Under section 127 of the Internal Revenue Code, up to $5,250 received in employer-provided educational assistance may be excluded from an employee s gross income. This educational benefit may be used at either the undergraduate or graduate level and may be used for payments for tuition, fees, books, supplies, and equipment. Unlike the business deduction for education-related expenses discussed later, with few exceptions education courses covered by section 127 may be either job-related or non-job-related. This exclusion for employer-provided educational assistance has its origins in the Revenue Act of 1978 (P.L ). Congress has extended this educational benefit many times over the last 30 years and most recently made the benefit permanent in 2013 as part of the American Taxpayer Relief Act of 2012 (P.L ). According to a 2010 study, close to 1 million employees annually benefit from employerprovided education assistance under section 127, and employees receiving this benefit have pursued their educations across various levels and academic disciplines. vi According to the same 2010 study, of the degrees pursued by beneficiaries in , 3 percent were at the certificate level, 26 percent were associate s degrees, 18 percent were bachelor s degrees, 36 percent were master s level degrees, 6 percent were other graduate level degrees, and 11 percent were not in a degree program. Employer-Provided Qualified Tuition Reduction (IRC Sec. 117) To attract and retain faculty and other employees, a number of institutions of higher education provide their employees and employees spouses and dependents with a benefit to study tuition-free or at a reduced rate of tuition. Additionally, to attract high-quality graduate students, institutions will often waive or reduce tuition if a graduate student teaches or conducts research for the institution. Section 117 of the IRC provides for tax-free treatment of

17 such qualified tuition reductions. As indicated below, different rules apply at the graduate level and at education below the graduate level.

18

19 Business Deduction for Work-Related Education Expenses (IRC Sec. 162) Employees who can itemize their deductions may be able to take a deduction for education expenses related to their work. To qualify for the deduction, the education must meet two tests. First, the education must be required by an employer or the law in order for the employee to keep his or her current salary, status, or job. Second, the education must maintain or improve skills needed in the employee s present work. An example of a qualifying workrelated education expense would be continuing education courses for certified public accountants. To maintain their license to practice, certified public accountants are required by law to take a given number of education courses each year. As the cost of college continued to escalate in the 1980s and 1990s, Congress turned to the tax code to create tax-preferred benefits for college savings. Over the years, Congress authorized two additional tax benefits for education savings a tax exclusion for interest earned on education savings accounts (529 Plans) and the waiving of the penalty on early withdrawals from Individual Retirement Accounts used to pay for qualified education expenses. 529 Plans (IRC Sec. 529) 529 plans, named after the section of Internal Revenue Code that stipulates their tax treatment, were created by the states as state-sponsored investment vehicles to encourage families to save for college. The specific federal tax benefit of 529 plans to families is that the distributions are tax-free if used to pay for qualified higher education expenses. The first such plan was created by the state of Michigan in Initial confusion regarding the tax treatment of these plans led the U.S. Congress to enact legislation to clarify their tax treatment. Congress first recognized 529 plans in the Small Business Job Protection Act of 1996 (P.L ) and made subsequent changes to them in 1997 under the Taxpayer Relief Act (P.L ). It should be noted that with respect to federal income taxes, these plans allowed for tax-free growth of investments, but distributions were fully taxable. In 2001, as part of a broader set of tax reforms, Congress made distributions tax-free and that rule was made

20 permanent in Two types of 529 plans exist prepaid tuition plans and college savings plans. While prepaid tuition and college savings plans have distinct differences, the federal tax treatment and benefit of these two types of plans is identical under both types of 529s, distributions and withdrawals are tax-free if the funds are used to pay for qualified higher education expenses. Under a prepaid 529 plan, a contributor (e.g., parent, grandparent, family friend) purchases a percentage of future tuition costs at current prices. The initial idea of the prepaid tuition plans was to provide families with a hedge against tuition inflation. Although prepaid tuition plans were the first type of 529 plan, the number of such plans has dropped considerably as skyrocketing tuition costs have ballooned future obligations. This has resulted in a decline in the popularity of prepaid 529 plans. There are currently 17 prepaid 529 plans and ninety 529 college savings plans across the nation. Under a 529 college savings plan, contributors invest in a portfolio of mutual funds, stocks, bonds, and other investments with the final value of the 529 account determined by the performance of the plan s investments. Many states offer a variety of 529 college savings plans some of which provide more aggressive investment opportunities as the beneficiary is younger and more conservative investments as the beneficiary approaches the age of enrolling in college. Over the last decade, the total assets in state-sponsored 529 plans has grown considerably, from $45 billion in 2003 to $224 billion in 2014 (in constant 2014 dollars). SOURCE: TRENDS IN STUDENT AID 2016

21 Average 529 Account Value in 2016 Dollars $25,000 $20,000 $15,000 $10,000 $5,000 $ SOURCE: COLLEGE SAVINGS PLAN NETWORK Additionally, in 2016, there were approximately 12.1 million 529 accounts with an average account value of $21,383. While the number of accounts and their assets have grown over time, still a very small number of American households have an account. According to the Federal Reserve s Survey of Consumer Finance, less than three percent of families save for college in a 529 or Coverdell account (discussed below). Further, those families with college savings plans are generally wealthier, having about three times the median income as families without a college savings account.

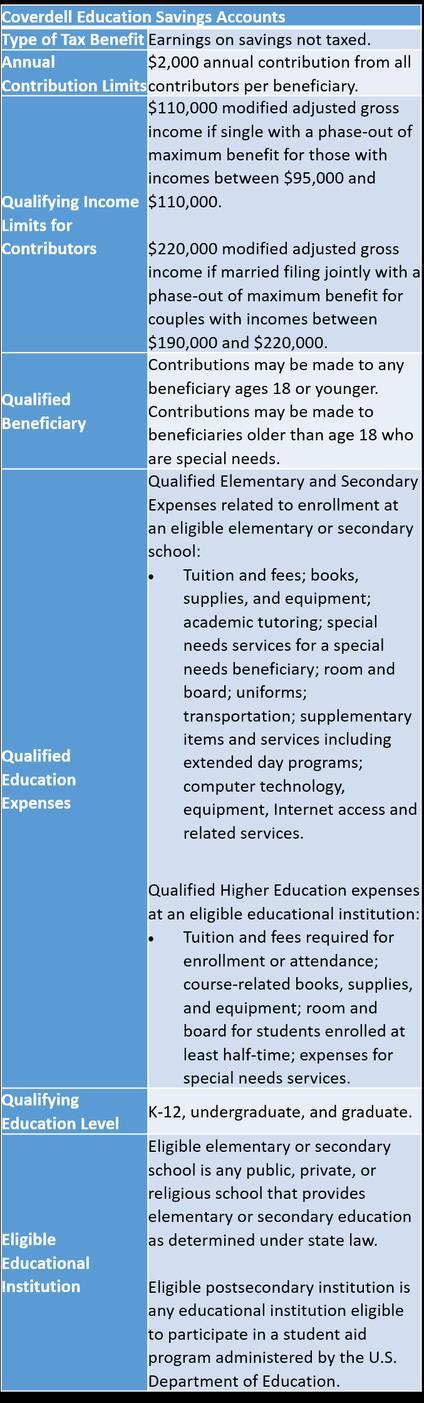

22 Coverdell Education Savings Accounts (IRC Sec. 530) Coverdell Education Savings Accounts, named after the late Senator Paul Coverdell (R-GA), are yet another tax-preferred savings vehicle for education. Similar to 529 plans, the investments in Coverdell accounts grow tax-free and the distributions are tax-free provided they are used for qualified education expenses. However, there are significant differences between the two. First, unlike 529 plans that are strictly for college education, a Coverdell can pay for education expenses at the elementary, secondary, or postsecondary levels. Additionally, unlike 529 plans that have no annual contribution limits to accounts and no income restrictions on contributors, Coverdell accounts limit annual account contributions to $2,000 and limit tax payers with an income of more than $110,000 (single)/$220,000 (joint) from making contributions. Finally, Coverdell accounts, a benefit provided for in the federal tax code, are neither state-sponsored nor state-run savings plans. Coverdell Savings Accounts were first created as part of the Taxpayer Relief Act of 1997 (P.L ) and were initially called Education IRAs. Most recently, the $2,000 annual contribution limit was made permanent as part of the American Taxpayer Relief Act of 2012 (P.L ). Barring such a change, the annual limit would have dropped to $500 in 2013.

23

24 Early Withdrawals from Individual Retirement Accounts (IRC Sec. 72(t)) Under normal circumstances, if an individual takes a distribution from an IRA Traditional or Roth before the age of 59 ½, the individual must pay a 10 percent penalty for the early distribution in addition to any regular income tax that is due. However, if the distribution is used to pay for qualified higher education expenses for the taxpayer, spouse, or dependents at any educational institution eligible to participate in a student aid program administered by the U.S. Department of Education, the 10 percent penalty is waived. Qualified education expenses are tuition, fees, books, supplies, and equipment required for attendance. If the student is enrolled on at least a half-time basis, room and board may be considered a qualified education expense. Updated June 2017 i U.S. Government Accountability Office (2012). Improved Tax Information Could Help Families Pay for College (GAO ). ii Delisle, Jason, and Kim Dancy. A New Look at Tuition Tax Benefits. Washington, DC, iii Ibid iv U.S. Government Accountability Office (2012). Improved Tax Information Could Help Families Pay for College (GAO ). v U.S. Internal Revenue Service (2014). Statement of Income Tax Stats Individual Statistical Tables by Size of Adjusted Gross Income. vi National Association of Independent Colleges and Universities & Society for Human Resource Management (2010). Who Benefits from Section 127: A Study of Employee Education Assistance Provided under Section 127 of the Internal Revenue Code.

Scholarship Reporting

Scholarship Reporting For tax purposes, scholarships are amounts that benefit an undergraduate or graduate student attending an educational institution in pursuit of a degree. Fellowships are amounts paid

Scholarship Reporting For tax purposes, scholarships are amounts that benefit an undergraduate or graduate student attending an educational institution in pursuit of a degree. Fellowships are amounts paid

Question No: 1 What must be considered with completing a needs analysis for a family saving for a child s tuition?

Volume: 443 Questions Question No: 1 What must be considered with completing a needs analysis for a family saving for a child s tuition? A. Where the child will go to college B. Where the family lives

Volume: 443 Questions Question No: 1 What must be considered with completing a needs analysis for a family saving for a child s tuition? A. Where the child will go to college B. Where the family lives

November 6, Re: Higher Education Provisions in H.R. 1, the Tax Cuts and Jobs Act. Dear Chairman Brady and Ranking Member Neal:

The Honorable Kevin Brady The Honorable Richard Neal Chairman Ranking Member Ways and Means Committee Ways and Means Committee United States House of Representatives United States House of Representatives

The Honorable Kevin Brady The Honorable Richard Neal Chairman Ranking Member Ways and Means Committee Ways and Means Committee United States House of Representatives United States House of Representatives

Trends in Student Aid and Trends in College Pricing

Trends in Student Aid and Trends in College Pricing 2012 NYSFAAA Conference Katrina Delgrosso Senior Educational Manager Agenda What is the College Board Advocacy & Policy Center? Trends in College Pricing

Trends in Student Aid and Trends in College Pricing 2012 NYSFAAA Conference Katrina Delgrosso Senior Educational Manager Agenda What is the College Board Advocacy & Policy Center? Trends in College Pricing

WASHINGTON COLLEGE SAVINGS

WASHINGTON COLLEGE SAVINGS EVERY CHILD DESERVES TO GO TITLE BUILDING STUDENT SUCCESS ONE DOLLAR AT A TIME Jacquelyne Ferrado WFAA Conference October 12, 2017 Presenters Event Date SESSION GOALS Raise Awareness

WASHINGTON COLLEGE SAVINGS EVERY CHILD DESERVES TO GO TITLE BUILDING STUDENT SUCCESS ONE DOLLAR AT A TIME Jacquelyne Ferrado WFAA Conference October 12, 2017 Presenters Event Date SESSION GOALS Raise Awareness

Fiscal Years [Millions of Dollars] Provision Effective

![Fiscal Years [Millions of Dollars] Provision Effective](/thumbs/71/65805895.jpg "Fiscal Years [Millions of Dollars] Provision Effective") JOINT COMMITTEE ON TAXATION December 3, 2014 JCX-107-14 R ESTIMATED REVENUE EFFECTS OF H.R. 5771, THE "TAX INCREASE PREVENTION ACT OF 2014," SCHEDULED FOR CONSIDERATION BY THE HOUSE OF REPRESENTATIVES

JOINT COMMITTEE ON TAXATION December 3, 2014 JCX-107-14 R ESTIMATED REVENUE EFFECTS OF H.R. 5771, THE "TAX INCREASE PREVENTION ACT OF 2014," SCHEDULED FOR CONSIDERATION BY THE HOUSE OF REPRESENTATIVES

GRADUATE STUDENTS Academic Year

Financial Aid Information for GRADUATE STUDENTS Academic Year 2017-2018 Your Financial Aid Award This booklet is designed to help you understand your financial aid award, policies for receiving aid and

Financial Aid Information for GRADUATE STUDENTS Academic Year 2017-2018 Your Financial Aid Award This booklet is designed to help you understand your financial aid award, policies for receiving aid and

UCLA Affordability. Ronald W. Johnson Director, Financial Aid Office. May 30, 2012

UCLA Affordability Ronald W. Johnson Director, Financial Aid Office May 30, 2012 1 UC is affordable First, Students must: Apply for admission in November File FAFSA and GPA Verification Form between January

UCLA Affordability Ronald W. Johnson Director, Financial Aid Office May 30, 2012 1 UC is affordable First, Students must: Apply for admission in November File FAFSA and GPA Verification Form between January

Master of Science in Taxation (M.S.T.) Program

Program") The W. Edwards Deming School of Business Master of Science in Taxation (M.S.T.) Program REV. 01-2017 CATALOG SUPPLEMENT (A Non-Resident Independent Study Degree Program) The University s School of Business

The W. Edwards Deming School of Business Master of Science in Taxation (M.S.T.) Program REV. 01-2017 CATALOG SUPPLEMENT (A Non-Resident Independent Study Degree Program) The University s School of Business

Is College Worth It? Understanding The Costs And Benefits of College

Is College Worth It? Understanding The Costs And Benefits of College Understanding the Costs & Benefits of College A lagging economy and skyrocketing university costs leave many Americans asking, Is college

Is College Worth It? Understanding The Costs And Benefits of College Understanding the Costs & Benefits of College A lagging economy and skyrocketing university costs leave many Americans asking, Is college

SCHOOL PERFORMANCE FACT SHEET CALENDAR YEARS 2014 & TECHNOLOGIES - 45 Months. On Time Completion Rates (Graduation Rates)

") SCHOOL PERFORMANCE FACT SHEET CALENDAR YEARS 2014 & 2015 On Time Completion Rates (Graduation Rates) Calendar Year Number of Students Who Began the Program Students Available for Graduation Number of On

SCHOOL PERFORMANCE FACT SHEET CALENDAR YEARS 2014 & 2015 On Time Completion Rates (Graduation Rates) Calendar Year Number of Students Who Began the Program Students Available for Graduation Number of On

Argosy University, Los Angeles MASTERS IN ORGANIZATIONAL LEADERSHIP - 20 Months School Performance Fact Sheet - Calendar Years 2014 & 2015

SCHOOL PERFORMANCE FACT SHEET CALENDAR YEARS 2014 & 2015 On Time Completion Rates (Graduation Rates) Calendar Year Number of Students Who Began the Program Students Available for Graduation Number of On

SCHOOL PERFORMANCE FACT SHEET CALENDAR YEARS 2014 & 2015 On Time Completion Rates (Graduation Rates) Calendar Year Number of Students Who Began the Program Students Available for Graduation Number of On

Trends in College Pricing

Trends in College Pricing 2009 T R E N D S I N H I G H E R E D U C A T I O N S E R I E S T R E N D S I N H I G H E R E D U C A T I O N S E R I E S Highlights Published Tuition and Fee and Room and Board

Trends in College Pricing 2009 T R E N D S I N H I G H E R E D U C A T I O N S E R I E S T R E N D S I N H I G H E R E D U C A T I O N S E R I E S Highlights Published Tuition and Fee and Room and Board

TRENDS IN. College Pricing

2008 TRENDS IN College Pricing T R E N D S I N H I G H E R E D U C A T I O N S E R I E S T R E N D S I N H I G H E R E D U C A T I O N S E R I E S Highlights 2 Published Tuition and Fee and Room and Board

2008 TRENDS IN College Pricing T R E N D S I N H I G H E R E D U C A T I O N S E R I E S T R E N D S I N H I G H E R E D U C A T I O N S E R I E S Highlights 2 Published Tuition and Fee and Room and Board

What You Need to Know About Financial Aid

What You Need to Know About Financial Aid 2018-2019 Topics We Will Discuss Tonight What is financial aid? Cost of attendance (COA) Expected family contribution (EFC) Financial need Categories, types, and

What You Need to Know About Financial Aid 2018-2019 Topics We Will Discuss Tonight What is financial aid? Cost of attendance (COA) Expected family contribution (EFC) Financial need Categories, types, and

How to Prepare for the Growing Price Tag

The Skyrocketing Cost of College How to Prepare for the Growing Price Tag Ken O Connor, Director of Student Advocacy, Fynanz, Inc. Mike Sabatino, CFP, Managing Director of Financial Planning and Education,

The Skyrocketing Cost of College How to Prepare for the Growing Price Tag Ken O Connor, Director of Student Advocacy, Fynanz, Inc. Mike Sabatino, CFP, Managing Director of Financial Planning and Education,

Availability of Grants Largely Offset Tuition Increases for Low-Income Students, U.S. Report Says

Wednesday, October 2, 2002 http://chronicle.com/daily/2002/10/2002100206n.htm Availability of Grants Largely Offset Tuition Increases for Low-Income Students, U.S. Report Says As the average price of attending

Wednesday, October 2, 2002 http://chronicle.com/daily/2002/10/2002100206n.htm Availability of Grants Largely Offset Tuition Increases for Low-Income Students, U.S. Report Says As the average price of attending

2010 DAVID LAMB PHOTOGRAPHY RIT/NTID FINANCIAL AID AND SCHOLARSHIPS

2010 DAVID LAMB PHOTOGRAPHY RIT/NTID FINANCIAL AID AND SCHOLARSHIPS An Exceptional Value An Outstanding Investment An Affordable Choice You ve decided that you re looking for the quality, reputation and

2010 DAVID LAMB PHOTOGRAPHY RIT/NTID FINANCIAL AID AND SCHOLARSHIPS An Exceptional Value An Outstanding Investment An Affordable Choice You ve decided that you re looking for the quality, reputation and

ATHLETIC ENDOWMENT FUND MOUNTAINEER ATHLETIC CLUB

ATHLETIC ENDOWMENT FUND MOUNTAINEER ATHLETIC CLUB The Athletic Endowment Fund provides donors with the unique opportunity to assist the West Virginia University Department of Intercollegiate Athletics

ATHLETIC ENDOWMENT FUND MOUNTAINEER ATHLETIC CLUB The Athletic Endowment Fund provides donors with the unique opportunity to assist the West Virginia University Department of Intercollegiate Athletics

Higher Education. Pennsylvania State System of Higher Education. November 3, 2017

November 3, 2017 Higher Education Pennsylvania s diverse higher education sector - consisting of many different kinds of public and private colleges and universities - helps students gain the knowledge

November 3, 2017 Higher Education Pennsylvania s diverse higher education sector - consisting of many different kinds of public and private colleges and universities - helps students gain the knowledge

An Introduction to School Finance in Texas

An Introduction to School Finance in Texas May 12, 2010 Sheryl Pace TTARA Research Foundation space@ttara.org (512) 472-8838 Texas Public Education System 1,300 school districts (#1 in the nation) 1,025

An Introduction to School Finance in Texas May 12, 2010 Sheryl Pace TTARA Research Foundation space@ttara.org (512) 472-8838 Texas Public Education System 1,300 school districts (#1 in the nation) 1,025

About the College Board. College Board Advocacy & Policy Center

15% 10 +5 0 5 Tuition and Fees 10 Appropriations per FTE ( Excluding Federal Stimulus Funds) 15% 1980-81 1981-82 1982-83 1983-84 1984-85 1985-86 1986-87 1987-88 1988-89 1989-90 1990-91 1991-92 1992-93

15% 10 +5 0 5 Tuition and Fees 10 Appropriations per FTE ( Excluding Federal Stimulus Funds) 15% 1980-81 1981-82 1982-83 1983-84 1984-85 1985-86 1986-87 1987-88 1988-89 1989-90 1990-91 1991-92 1992-93

DEPARTMENT OF ART. Graduate Associate and Graduate Fellows Handbook

DEPARTMENT OF ART Graduate Associate and Graduate Fellows Handbook June 2016 Table of Contents Introduction-Graduate Associates... 3 Graduate Associate Responsibilities... 4 A. Graduate Teaching Associate

DEPARTMENT OF ART Graduate Associate and Graduate Fellows Handbook June 2016 Table of Contents Introduction-Graduate Associates... 3 Graduate Associate Responsibilities... 4 A. Graduate Teaching Associate

Series IV - Financial Management and Marketing Fiscal Year

Series IV - Financial Management and Marketing... 1 4.101 Fiscal Year... 1 4.102 Budget Preparation... 2 4.201 Authorized Signatures... 3 4.2021 Financial Assistance... 4 4.2021-R Financial Assistance

Series IV - Financial Management and Marketing... 1 4.101 Fiscal Year... 1 4.102 Budget Preparation... 2 4.201 Authorized Signatures... 3 4.2021 Financial Assistance... 4 4.2021-R Financial Assistance

Financing Education In Minnesota

Financing Education In Minnesota 2016-2017 Created with Tagul.com A Publication of the Minnesota House of Representatives Fiscal Analysis Department August 2016 Financing Education in Minnesota 2016-17

Financing Education In Minnesota 2016-2017 Created with Tagul.com A Publication of the Minnesota House of Representatives Fiscal Analysis Department August 2016 Financing Education in Minnesota 2016-17

Federal Update. Angela Smith, Training Officer U.S. Dept. of ED, Federal Student Aid WHITE HOUSE STUDENT LOAN INITIATIVES

Federal Update 1 WHITE HOUSE STUDENT LOAN INITIATIVES 2 SPECIAL DIRECT CONSOLIDATION LOANS 3 For Discussion/Training purposes ONLY. 1 Regular Direct Consolidation Loan Borrowers with any federal student

Federal Update 1 WHITE HOUSE STUDENT LOAN INITIATIVES 2 SPECIAL DIRECT CONSOLIDATION LOANS 3 For Discussion/Training purposes ONLY. 1 Regular Direct Consolidation Loan Borrowers with any federal student

Guidelines for Mobilitas Pluss postdoctoral grant applications

Annex 1 APPROVED by the Management Board of the Estonian Research Council on 23 March 2016, Directive No. 1-1.4/16/63 Guidelines for Mobilitas Pluss postdoctoral grant applications 1. Scope The guidelines

Annex 1 APPROVED by the Management Board of the Estonian Research Council on 23 March 2016, Directive No. 1-1.4/16/63 Guidelines for Mobilitas Pluss postdoctoral grant applications 1. Scope The guidelines

UCB Administrative Guidelines for Endowed Chairs

UCB Administrative Guidelines for Endowed Chairs I. General A. Purpose An endowed chair provides funds to a chair holder in support of his or her teaching, research, and service, and is supported by a

UCB Administrative Guidelines for Endowed Chairs I. General A. Purpose An endowed chair provides funds to a chair holder in support of his or her teaching, research, and service, and is supported by a

Financial aid: Degree-seeking undergraduates, FY15-16 CU-Boulder Office of Data Analytics, Institutional Research March 2017

CU-Boulder financial aid, degree-seeking undergraduates, FY15-16 Page 1 Financial aid: Degree-seeking undergraduates, FY15-16 CU-Boulder Office of Data Analytics, Institutional Research March 2017 Contents

CU-Boulder financial aid, degree-seeking undergraduates, FY15-16 Page 1 Financial aid: Degree-seeking undergraduates, FY15-16 CU-Boulder Office of Data Analytics, Institutional Research March 2017 Contents

HAMILTON. Viewing Education Loans Through A Myopic Lens PROJECT. The Brookings Institution. Advancing Opportunity, Prosperity and Growth

THE HAMILTON PROJECT Advancing Opportunity, Prosperity and Growth D I S C U S S I O N P A P E R 2 0 0 8-0 5 J U N E 2 0 0 8 Sima J. Gandhi Viewing Education Loans Through A Myopic Lens The Brookings Institution

THE HAMILTON PROJECT Advancing Opportunity, Prosperity and Growth D I S C U S S I O N P A P E R 2 0 0 8-0 5 J U N E 2 0 0 8 Sima J. Gandhi Viewing Education Loans Through A Myopic Lens The Brookings Institution

Financial Aid. Financial Aid. Course Descriptions

Monmouth University believes that financing a student s education should be a cooperative effort between the student and the institution. To that end, the staff of the Financial Aid Office is available

Monmouth University believes that financing a student s education should be a cooperative effort between the student and the institution. To that end, the staff of the Financial Aid Office is available

STUDENT 16/17 FUNDING GUIDE LOANS & GRANTS FOR FULL-TIME POST-SECONDARY STUDIES

STUDENT LOANS & GRANTS FUNDING GUIDE FOR FULL-TIME POST-SECONDARY STUDIES 16/17 CONTENTS The information and amounts in the Student Loans & Grants Funding Guide are current as of June 2016. All amounts

STUDENT LOANS & GRANTS FUNDING GUIDE FOR FULL-TIME POST-SECONDARY STUDIES 16/17 CONTENTS The information and amounts in the Student Loans & Grants Funding Guide are current as of June 2016. All amounts

VERIFICATION POLICY STUDENT FINANCIAL SERVICES WASHINGTON STATE UNIVERSITY

VERIFICATION POLICY STUDENT FINANCIAL SERVICES WASHINGTON STATE UNIVERSITY 2017-2018 Verification Purpose: Reviewing a student s file often involves more than just the verification process. File review

VERIFICATION POLICY STUDENT FINANCIAL SERVICES WASHINGTON STATE UNIVERSITY 2017-2018 Verification Purpose: Reviewing a student s file often involves more than just the verification process. File review

Trends in Tuition at Idaho s Public Colleges and Universities: Critical Context for the State s Education Goals

1 Trends in Tuition at Idaho s Public Colleges and Universities: Critical Context for the State s Education Goals June 2017 Idahoans have long valued public higher education, recognizing its importance

1 Trends in Tuition at Idaho s Public Colleges and Universities: Critical Context for the State s Education Goals June 2017 Idahoans have long valued public higher education, recognizing its importance

Student Aid Alberta Operational Policy and Procedure Manual Aug 1, 2016 July 31, 2017

Operational Policy and Procedure Manual Revised: Nov 1, 2016 Summary of Changes 2016-17 Student Aid Alberta will periodically revise the Operational Policy and Procedure Manual. A summary of the most significant

Operational Policy and Procedure Manual Revised: Nov 1, 2016 Summary of Changes 2016-17 Student Aid Alberta will periodically revise the Operational Policy and Procedure Manual. A summary of the most significant

In 2010, the Teach Plus-Indianapolis Teaching Policy Fellows, a cohort of early career educators teaching

Introduction Dollars and Sense: Elevating the teaching profession by leveraging talent In 2010, the Teach Plus-Indianapolis Teaching Policy Fellows, a cohort of early career educators teaching in low-income

Introduction Dollars and Sense: Elevating the teaching profession by leveraging talent In 2010, the Teach Plus-Indianapolis Teaching Policy Fellows, a cohort of early career educators teaching in low-income

HOUSE OF REPRESENTATIVES AS REVISED BY THE COMMITTEE ON EDUCATION APPROPRIATIONS ANALYSIS

BILL #: HB 269 HOUSE OF REPRESENTATIVES AS REVISED BY THE COMMITTEE ON EDUCATION APPROPRIATIONS ANALYSIS RELATING TO: SPONSOR(S): School District Best Financial Management Practices Reviews Representatives

BILL #: HB 269 HOUSE OF REPRESENTATIVES AS REVISED BY THE COMMITTEE ON EDUCATION APPROPRIATIONS ANALYSIS RELATING TO: SPONSOR(S): School District Best Financial Management Practices Reviews Representatives

Summary of Special Provisions & Money Report Conference Budget July 30, 2014 Updated July 31, 2014

6.4 (b) Base Budget This changes how average daily membership is built in the Budget. Until now, projected ADM increases have been included in the continuation budget. This special provision defines what

6.4 (b) Base Budget This changes how average daily membership is built in the Budget. Until now, projected ADM increases have been included in the continuation budget. This special provision defines what

DUAL ENROLLMENT ADMISSIONS APPLICATION. You can get anywhere from here.

DUAL ENROLLMENT ADMISSIONS APPLICATION SM You can get anywhere from here. Please print or type: DUAL ENROLLMENT APPLICATION Last Name First Name Maiden/Middle Social Security # Local Address (include apt.

DUAL ENROLLMENT ADMISSIONS APPLICATION SM You can get anywhere from here. Please print or type: DUAL ENROLLMENT APPLICATION Last Name First Name Maiden/Middle Social Security # Local Address (include apt.

Grant/Scholarship General Criteria CRITERIA TO APPLY FOR AN AESF GRANT/SCHOLARSHIP

2017-2018 Grant/Scholarship General Criteria CRITERIA TO APPLY FOR AN AESF GRANT/SCHOLARSHIP 1) Student(s) must attend an AESF member Episcopal school 2) An AESF Grant/Scholarship Application and supporting

2017-2018 Grant/Scholarship General Criteria CRITERIA TO APPLY FOR AN AESF GRANT/SCHOLARSHIP 1) Student(s) must attend an AESF member Episcopal school 2) An AESF Grant/Scholarship Application and supporting

Paying for College. Marla Lewis Office of Student Financial Aid

Paying for College Marla Lewis Office of Student Financial Aid What is financial aid? Financial Aid is any resource that can assist in offsetting the cost of attending college. What are the sources of

Paying for College Marla Lewis Office of Student Financial Aid What is financial aid? Financial Aid is any resource that can assist in offsetting the cost of attending college. What are the sources of

Data Glossary. Summa Cum Laude: the top 2% of each college's distribution of cumulative GPAs for the graduating cohort. Academic Honors (Latin Honors)

") Institutional Research and Assessment Data Glossary This document is a collection of terms and variable definitions commonly used in the universities reports. The definitions were compiled from various

Institutional Research and Assessment Data Glossary This document is a collection of terms and variable definitions commonly used in the universities reports. The definitions were compiled from various

Options for Tuition Rates for 2016/17 Please select one from the following options, sign and return to the CFO

Options for Tuition Rates for 2016/17 Please select one from the following options, sign and return to the CFO Family Name Student(s) Name(s) Option #1: The Governors Club rate is $17,145 and reflects

Options for Tuition Rates for 2016/17 Please select one from the following options, sign and return to the CFO Family Name Student(s) Name(s) Option #1: The Governors Club rate is $17,145 and reflects

Differential Tuition Budget Proposal FY

Differential Tuition Budget Proposal FY 2013-2014 MPA Differential Tuition Subcommittee MPA Faculty This document presents the budget proposal of the MPA Differential Tuition Subcommittee (MPADTS) for

Differential Tuition Budget Proposal FY 2013-2014 MPA Differential Tuition Subcommittee MPA Faculty This document presents the budget proposal of the MPA Differential Tuition Subcommittee (MPADTS) for

2014 State Residency Conference Frequently Asked Questions FAQ Categories

2014 State Residency Conference Frequently Asked Questions FAQ Categories Deadline... 2 The Five Year Rule... 3 Statutory Grace Period... 4 Immigration... 5 Active Duty Military... 7 Spouse Benefit...

2014 State Residency Conference Frequently Asked Questions FAQ Categories Deadline... 2 The Five Year Rule... 3 Statutory Grace Period... 4 Immigration... 5 Active Duty Military... 7 Spouse Benefit...

Alex Robinson Financial Aid

Alex Robinson Financial Aid Image Source: https://www.google.com/search?q=college+decisions+and+financial+fit&espv=2&biw=1366&bih=643&source=lnms&tb m=isch&sa=x&ved=0cagq_auoa2ovchmi6vt40tknxwivee6ich2ipgcw#imgrc=45cmbyr3nan8gm%3a

Alex Robinson Financial Aid Image Source: https://www.google.com/search?q=college+decisions+and+financial+fit&espv=2&biw=1366&bih=643&source=lnms&tb m=isch&sa=x&ved=0cagq_auoa2ovchmi6vt40tknxwivee6ich2ipgcw#imgrc=45cmbyr3nan8gm%3a

Invest in CUNY Community Colleges

Invest in Opportunity Invest in CUNY Community Colleges Pat Arnow Professional Staff Congress Invest in Opportunity Household Income of CUNY Community College Students

Invest in Opportunity Invest in CUNY Community Colleges Pat Arnow Professional Staff Congress Invest in Opportunity Household Income of CUNY Community College Students

Guidelines for Mobilitas Pluss top researcher grant applications

Annex 1 APPROVED by the Management Board of the Estonian Research Council on 23 March 2016, Directive No. 1-1.4/16/63 Guidelines for Mobilitas Pluss top researcher grant applications 1. Scope The guidelines

Annex 1 APPROVED by the Management Board of the Estonian Research Council on 23 March 2016, Directive No. 1-1.4/16/63 Guidelines for Mobilitas Pluss top researcher grant applications 1. Scope The guidelines

The Colorado Promise

The Colorado Promise The Colorado Promise ensures that every Coloradan who is willing to work for it can develop the skills they need to find opportunity in the new economy. The Challenge Ahead We find

The Colorado Promise The Colorado Promise ensures that every Coloradan who is willing to work for it can develop the skills they need to find opportunity in the new economy. The Challenge Ahead We find

FINANCING YOUR COLLEGE EDUCATION

FINANCING YOUR COLLEGE EDUCATION Columbia High School October 4, 2017 Presenter Douglas Wilson Kean University 1 Overview Types of Assistance Scholarship Information Applying for Need-Based Aid Eligibility

FINANCING YOUR COLLEGE EDUCATION Columbia High School October 4, 2017 Presenter Douglas Wilson Kean University 1 Overview Types of Assistance Scholarship Information Applying for Need-Based Aid Eligibility

EDUCATIONAL ATTAINMENT

EDUCATIONAL ATTAINMENT By 2030, at least 60 percent of Texans ages 25 to 34 will have a postsecondary credential or degree. Target: Increase the percent of Texans ages 25 to 34 with a postsecondary credential.

EDUCATIONAL ATTAINMENT By 2030, at least 60 percent of Texans ages 25 to 34 will have a postsecondary credential or degree. Target: Increase the percent of Texans ages 25 to 34 with a postsecondary credential.

Paying for. Cosmetology School S C H O O L B E AU T Y. Financing your new life. beautyschoolnetwork.com pg 1

Paying for Cosmetology School B E AU T Y S C H O O L Financing your new life. beautyschoolnetwork.com beautyschoolnetwork.com pg 1 B E AU T Y S C H O O L Table of Contents How to Pay for Cosmetology School...

Paying for Cosmetology School B E AU T Y S C H O O L Financing your new life. beautyschoolnetwork.com beautyschoolnetwork.com pg 1 B E AU T Y S C H O O L Table of Contents How to Pay for Cosmetology School...

Modern Trends in Higher Education Funding. Tilea Doina Maria a, Vasile Bleotu b

Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Scien ce s 116 ( 2014 ) 2226 2230 Abstract 5 th World Conference on Educational Sciences - WCES 2013 Modern Trends

Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Scien ce s 116 ( 2014 ) 2226 2230 Abstract 5 th World Conference on Educational Sciences - WCES 2013 Modern Trends

Qs&As Providing Financial Aid to Former Everest College Students March 11, 2015

Qs&As Providing Financial Aid to Former Everest College Students March 11, 2015 Q. How is the government helping students affected by the closure of Everest College? A. Ontario is providing financial assistance

Qs&As Providing Financial Aid to Former Everest College Students March 11, 2015 Q. How is the government helping students affected by the closure of Everest College? A. Ontario is providing financial assistance

NATIVE VILLAGE OF BARROW WORKFORCE DEVLEOPMENT DEPARTMENT HIGHER EDUCATION AND ADULT VOCATIONAL TRAINING FINANCIAL ASSISTANCE APPLICATION

NATIVE VILLAGE OF BARROW WORKFORCE DEVLEOPMENT DEPARTMENT HIGHER EDUCATION AND ADULT VOCATIONAL TRAINING FINANCIAL ASSISTANCE APPLICATION To better assist our Clients, here is a check off list of the following

NATIVE VILLAGE OF BARROW WORKFORCE DEVLEOPMENT DEPARTMENT HIGHER EDUCATION AND ADULT VOCATIONAL TRAINING FINANCIAL ASSISTANCE APPLICATION To better assist our Clients, here is a check off list of the following

FORT HAYS STATE UNIVERSITY AT DODGE CITY

FORT HAYS STATE UNIVERSITY AT DODGE CITY INTRODUCTION Economic prosperity for individuals and the state relies on an educated workforce. For Kansans to succeed in the workforce, they must have an education

FORT HAYS STATE UNIVERSITY AT DODGE CITY INTRODUCTION Economic prosperity for individuals and the state relies on an educated workforce. For Kansans to succeed in the workforce, they must have an education

CHAPTER XI DIRECT TESTIMONY OF REGINALD M. AUSTRIA ON BEHALF OF SOUTHERN CALIFORNIA GAS COMPANY AND SAN DIEGO GAS & ELECTRIC COMPANY

Application No: A.1-09-00 Exhibit No.: Witness: R. Austria Application of Southern California Gas Company (U 90 G) and San Diego Gas & Electric Company (U 90 G) to Recover Costs Recorded in the Pipeline

Application No: A.1-09-00 Exhibit No.: Witness: R. Austria Application of Southern California Gas Company (U 90 G) and San Diego Gas & Electric Company (U 90 G) to Recover Costs Recorded in the Pipeline

IN-STATE TUITION PETITION INSTRUCTIONS AND DEADLINES Western State Colorado University

IN-STATE TUITION PETITION INSTRUCTIONS AND DEADLINES Western State Colorado University Petitions will be accepted beginning 60 days before the semester starts for each academic semester. Petitions will

IN-STATE TUITION PETITION INSTRUCTIONS AND DEADLINES Western State Colorado University Petitions will be accepted beginning 60 days before the semester starts for each academic semester. Petitions will

Michigan and Ohio K-12 Educational Financing Systems: Equality and Efficiency. Michael Conlin Michigan State University

Michigan and Ohio K-12 Educational Financing Systems: Equality and Efficiency Michael Conlin Michigan State University Paul Thompson Michigan State University October 2013 Abstract This paper considers

Michigan and Ohio K-12 Educational Financing Systems: Equality and Efficiency Michael Conlin Michigan State University Paul Thompson Michigan State University October 2013 Abstract This paper considers

RESIDENCY POLICY. Council on Postsecondary Education State of Rhode Island and Providence Plantations

S-5.0 RESIDENCY POLICY Council on Postsecondary Education State of Rhode Island and Providence Plantations Adopted: Amended: 12/02/1971 (BR) 05/22/1980 (BR) 07/02/1981 (BG) 04/15/1993 (BG) 09/27/1995 (BG)

S-5.0 RESIDENCY POLICY Council on Postsecondary Education State of Rhode Island and Providence Plantations Adopted: Amended: 12/02/1971 (BR) 05/22/1980 (BR) 07/02/1981 (BG) 04/15/1993 (BG) 09/27/1995 (BG)

Trends in Higher Education Series. Trends in College Pricing 2016

Trends in Higher Education Series Trends in College Pricing 2016 See the Trends in Higher Education website at trends.collegeboard.org for figures and tables in this report and for more information and

Trends in Higher Education Series Trends in College Pricing 2016 See the Trends in Higher Education website at trends.collegeboard.org for figures and tables in this report and for more information and

Arkansas Private Option Medicaid expansion is putting state taxpayers on the hook for millions in cost overruns

Arkansas Private Option Medicaid expansion is putting state taxpayers on the hook for millions in cost overruns ObamaCare advocates repeatedly promise that Medicaid expansion is fully funded by the federal

Arkansas Private Option Medicaid expansion is putting state taxpayers on the hook for millions in cost overruns ObamaCare advocates repeatedly promise that Medicaid expansion is fully funded by the federal

Financial Aid & Merit Scholarships Workshop

Financial Aid & Merit Scholarships Workshop www.admissions.umd.edu ApplyMaryland@umd.edu 301.314.8385 1.800.422.5867 Merit Scholarship Review James B. Massey Jr. Office of Undergraduate Admissions Financing

Financial Aid & Merit Scholarships Workshop www.admissions.umd.edu ApplyMaryland@umd.edu 301.314.8385 1.800.422.5867 Merit Scholarship Review James B. Massey Jr. Office of Undergraduate Admissions Financing

I. General provisions. II. Rules for the distribution of funds of the Financial Aid Fund for students

Rules and Regulations for the calculation, awarding and payment of financial aid for full-time and part-time students with awarding criteria and procedures at the Warsaw Film School I. General provisions

Rules and Regulations for the calculation, awarding and payment of financial aid for full-time and part-time students with awarding criteria and procedures at the Warsaw Film School I. General provisions

EDUCATIONAL ATTAINMENT

EDUCATIONAL ATTAINMENT By 2030, at least 60 percent of Texans ages 25 to 34 will have a postsecondary credential or degree. Target: Increase the percent of Texans ages 25 to 34 with a postsecondary credential.

EDUCATIONAL ATTAINMENT By 2030, at least 60 percent of Texans ages 25 to 34 will have a postsecondary credential or degree. Target: Increase the percent of Texans ages 25 to 34 with a postsecondary credential.

Value of Athletics in Higher Education March Prepared by Edward J. Ray, President Oregon State University

Materials linked from the 5/12/09 OSU Faculty Senate agenda 1. Who Participates Value of Athletics in Higher Education March 2009 Prepared by Edward J. Ray, President Oregon State University Today, more

Materials linked from the 5/12/09 OSU Faculty Senate agenda 1. Who Participates Value of Athletics in Higher Education March 2009 Prepared by Edward J. Ray, President Oregon State University Today, more

SCICU Legislative Strategic Plan 2018

The primary objective of the South Carolina Independent Colleges and Universities Legislative Strategic Plan is to establish an agenda and course of action for a program of education and advocacy on matters

The primary objective of the South Carolina Independent Colleges and Universities Legislative Strategic Plan is to establish an agenda and course of action for a program of education and advocacy on matters

STATE CAPITAL SPENDING ON PK 12 SCHOOL FACILITIES NORTH CAROLINA

STATE CAPITAL SPENDING ON PK 12 SCHOOL FACILITIES NORTH CAROLINA NOVEMBER 2010 Authors Mary Filardo Stephanie Cheng Marni Allen Michelle Bar Jessie Ulsoy 21st Century School Fund (21CSF) Founded in 1994,

STATE CAPITAL SPENDING ON PK 12 SCHOOL FACILITIES NORTH CAROLINA NOVEMBER 2010 Authors Mary Filardo Stephanie Cheng Marni Allen Michelle Bar Jessie Ulsoy 21st Century School Fund (21CSF) Founded in 1994,

Teaching Financial Literacy to Adult Students: Different Strokes for Different Folks

Teaching Financial Literacy to Adult Students: Different Strokes for Different Folks There is a gap between how adults perceive their financial knowledge and how they test out Source: FINRA Investor Education

Teaching Financial Literacy to Adult Students: Different Strokes for Different Folks There is a gap between how adults perceive their financial knowledge and how they test out Source: FINRA Investor Education

CHAPTER XXIV JAMES MADISON MEMORIAL FELLOWSHIP FOUNDATION

CHAPTER XXIV JAMES MADISON MEMORIAL FELLOWSHIP FOUNDATION Part Page 2400 Fellowship Program requirements... 579 2490 Enforcement of nondiscrimination on the basis of handicap in programs or activities

CHAPTER XXIV JAMES MADISON MEMORIAL FELLOWSHIP FOUNDATION Part Page 2400 Fellowship Program requirements... 579 2490 Enforcement of nondiscrimination on the basis of handicap in programs or activities

A Financial Model to Support the Future of The California State University

A Financial Model to Support the Future of The California State University Report of the Chancellor s Task Force for a Sustainable Financial Model for the CSU LETTER TO CHANCELLOR FROM THE CO-CHAIRS The

A Financial Model to Support the Future of The California State University Report of the Chancellor s Task Force for a Sustainable Financial Model for the CSU LETTER TO CHANCELLOR FROM THE CO-CHAIRS The

Chris George Dean of Admissions and Financial Aid St. Olaf College

Chris George Dean of Admissions and Financial Aid St. Olaf College 1. Apply for a FSA ID 2. Collect the documents you ll need and File the FAFSA 3. File other materials, if required 4. Research scholarship

Chris George Dean of Admissions and Financial Aid St. Olaf College 1. Apply for a FSA ID 2. Collect the documents you ll need and File the FAFSA 3. File other materials, if required 4. Research scholarship

Massachusetts Department of Elementary and Secondary Education. Title I Comparability

Massachusetts Department of Elementary and Secondary Education Title I Comparability 2009-2010 Title I provides federal financial assistance to school districts to provide supplemental educational services

Massachusetts Department of Elementary and Secondary Education Title I Comparability 2009-2010 Title I provides federal financial assistance to school districts to provide supplemental educational services

UNIVERSITY OF UTAH VETERANS SUPPORT CENTER

UNIVERSITY OF UTAH VETERANS SUPPORT CENTER ANNUAL REPORT 2015 2016 Overview The (VSC) continues to be utilized as a place for student veterans to find services, support, and camaraderie. The services include

UNIVERSITY OF UTAH VETERANS SUPPORT CENTER ANNUAL REPORT 2015 2016 Overview The (VSC) continues to be utilized as a place for student veterans to find services, support, and camaraderie. The services include

Suggested Citation: Institute for Research on Higher Education. (2016). College Affordability Diagnosis: Maine. Philadelphia, PA: Institute for

. College Affordability Diagnosis: Maine. Philadelphia, PA: Institute for") MAINE Suggested Citation: Institute for Research on Higher Education. (2016). College Affordability Diagnosis: Maine. Philadelphia, PA: Institute for Research on Higher Education, Graduate School of Education,

MAINE Suggested Citation: Institute for Research on Higher Education. (2016). College Affordability Diagnosis: Maine. Philadelphia, PA: Institute for Research on Higher Education, Graduate School of Education,

PRINCE GEORGE'S COMMUNITY COLLEGE OFFICE OF STUDENT FINANCIAL AID GUIDELINES FOR THE EDWARD T. CONROY MEMORIAL SCHOLARSHIP PROGRAM

PRINCE GEORGE'S COMMUNITY COLLEGE OFFICE OF STUDENT FINANCIAL AID GUIDELINES FOR THE EDWARD T. CONROY MEMORIAL SCHOLARSHIP PROGRAM APPROVED: June 13, 2007 Guidelines for the Edward T. Conroy Memorial Scholarship

PRINCE GEORGE'S COMMUNITY COLLEGE OFFICE OF STUDENT FINANCIAL AID GUIDELINES FOR THE EDWARD T. CONROY MEMORIAL SCHOLARSHIP PROGRAM APPROVED: June 13, 2007 Guidelines for the Edward T. Conroy Memorial Scholarship

Banner Financial Aid Release Guide. Release and June 2017

Banner Financial Aid Release Guide Release 8.29.1 and 9.3.3 June 2017 Notices Notices 2017 Ellucian. Contains confidential and proprietary information of Ellucian and its subsidiaries. Use of these materials

Banner Financial Aid Release Guide Release 8.29.1 and 9.3.3 June 2017 Notices Notices 2017 Ellucian. Contains confidential and proprietary information of Ellucian and its subsidiaries. Use of these materials

The Racial Wealth Gap

The Racial Wealth Gap Why Policy Matters by Laura Sullivan, Tatjana Meschede, Lars Dietrich, & Thomas Shapiro institute for assets & social policy, brandeis university Amy Traub, Catherine Ruetschlin &

The Racial Wealth Gap Why Policy Matters by Laura Sullivan, Tatjana Meschede, Lars Dietrich, & Thomas Shapiro institute for assets & social policy, brandeis university Amy Traub, Catherine Ruetschlin &

House Finance Committee Unveils Substitute Budget Bill

April 28, 2017 House Finance Committee Unveils Substitute Budget Bill On Tuesday, April 25, the House Finance Committee adopted a substitute version of House Bill 49, the budget bill for Fiscal Years (FY)

April 28, 2017 House Finance Committee Unveils Substitute Budget Bill On Tuesday, April 25, the House Finance Committee adopted a substitute version of House Bill 49, the budget bill for Fiscal Years (FY)

ILLINOIS DISTRICT REPORT CARD

-6-525-2- HAZEL CREST SD 52-5 HAZEL CREST SD 52-5 HAZEL CREST, ILLINOIS and federal laws require public school districts to release report cards to the public each year. 2 7 ILLINOIS DISTRICT REPORT CARD

-6-525-2- HAZEL CREST SD 52-5 HAZEL CREST SD 52-5 HAZEL CREST, ILLINOIS and federal laws require public school districts to release report cards to the public each year. 2 7 ILLINOIS DISTRICT REPORT CARD

Executive Summary. Laurel County School District. Dr. Doug Bennett, Superintendent 718 N Main St London, KY

Dr. Doug Bennett, Superintendent 718 N Main St London, KY 40741-1222 Document Generated On January 13, 2014 TABLE OF CONTENTS Introduction 1 Description of the School System 2 System's Purpose 4 Notable

Dr. Doug Bennett, Superintendent 718 N Main St London, KY 40741-1222 Document Generated On January 13, 2014 TABLE OF CONTENTS Introduction 1 Description of the School System 2 System's Purpose 4 Notable

MANAGEMENT CHARTER OF THE FOUNDATION HET RIJNLANDS LYCEUM

MANAGEMENT CHARTER OF THE FOUNDATION HET RIJNLANDS LYCEUM Article 1. Definitions. 1.1 This management charter uses the following definitions: (a) the Executive Board : the Executive Board of the Foundation,

MANAGEMENT CHARTER OF THE FOUNDATION HET RIJNLANDS LYCEUM Article 1. Definitions. 1.1 This management charter uses the following definitions: (a) the Executive Board : the Executive Board of the Foundation,

DEPARTMENT OF FINANCE AND ECONOMICS

Department of Finance and Economics 1 DEPARTMENT OF FINANCE AND ECONOMICS McCoy Hall Room 504 T: 512.245.2547 F: 512.245.3089 www.fin-eco.mccoy.txstate.edu (http://www.fin-eco.mccoy.txstate.edu) The mission

Department of Finance and Economics 1 DEPARTMENT OF FINANCE AND ECONOMICS McCoy Hall Room 504 T: 512.245.2547 F: 512.245.3089 www.fin-eco.mccoy.txstate.edu (http://www.fin-eco.mccoy.txstate.edu) The mission

Table of Contents Welcome to the Federal Work Study (FWS)/Community Service/America Reads program.

/Community Service/America Reads program.") Table of Contents Welcome........................................ 1 Basic Requirements for the Federal Work Study (FWS)/ Community Service/America Reads program............ 2 Responsibilities of All Participants

Table of Contents Welcome........................................ 1 Basic Requirements for the Federal Work Study (FWS)/ Community Service/America Reads program............ 2 Responsibilities of All Participants

ILLINOIS DISTRICT REPORT CARD

-6-525-2- Hazel Crest SD 52-5 Hazel Crest SD 52-5 Hazel Crest, ILLINOIS 2 8 ILLINOIS DISTRICT REPORT CARD and federal laws require public school districts to release report cards to the public each year.

-6-525-2- Hazel Crest SD 52-5 Hazel Crest SD 52-5 Hazel Crest, ILLINOIS 2 8 ILLINOIS DISTRICT REPORT CARD and federal laws require public school districts to release report cards to the public each year.

1.0 INTRODUCTION. The purpose of the Florida school district performance review is to identify ways that a designated school district can:

1.0 INTRODUCTION 1.1 Overview Section 11.515, Florida Statutes, was created by the 1996 Florida Legislature for the purpose of conducting performance reviews of school districts in Florida. The statute

1.0 INTRODUCTION 1.1 Overview Section 11.515, Florida Statutes, was created by the 1996 Florida Legislature for the purpose of conducting performance reviews of school districts in Florida. The statute

The Ohio State University Library System Improvement Request,

The Ohio State University Library System Improvement Request, 2005-2009 Introduction: A Cooperative System with a Common Mission The University, Moritz Law and Prior Health Science libraries have a long

The Ohio State University Library System Improvement Request, 2005-2009 Introduction: A Cooperative System with a Common Mission The University, Moritz Law and Prior Health Science libraries have a long

Draft Budget : Higher Education

The Scottish Parliament and Scottish Parliament Infor mation C entre l ogos. SPICe Briefing Draft Budget 2015-16: Higher Education 6 November 2014 14/79 Suzi Macpherson This briefing reports on funding

The Scottish Parliament and Scottish Parliament Infor mation C entre l ogos. SPICe Briefing Draft Budget 2015-16: Higher Education 6 November 2014 14/79 Suzi Macpherson This briefing reports on funding

Global Television Manufacturing Industry : Trend, Profit, and Forecast Analysis Published September 2012

Industry 2012-2017: Published September 2012 Lucintel, a premier global management consulting and market research firm creates your equation for growth whether you need to understand market dynamics, identify

Industry 2012-2017: Published September 2012 Lucintel, a premier global management consulting and market research firm creates your equation for growth whether you need to understand market dynamics, identify

A New Compact for Higher Education in Virginia

October 22, 2003 A New Compact for Higher Education in Virginia Robert B. Archibald David H. Feldman College of William and Mary 1. Introduction This brief paper describes a plan to restructure the relationship

October 22, 2003 A New Compact for Higher Education in Virginia Robert B. Archibald David H. Feldman College of William and Mary 1. Introduction This brief paper describes a plan to restructure the relationship

Music Chapel House Rules and Policies hapelle Musicale Reine Elisabeth, fondation d'utilité publique

1 Music Chapel The Queen Elisabeth Music Chapel endeavors to make access to the Music Chapel possible for all students meeting the artistic admission requirements. Admission to the Music Chapel is based

1 Music Chapel The Queen Elisabeth Music Chapel endeavors to make access to the Music Chapel possible for all students meeting the artistic admission requirements. Admission to the Music Chapel is based

Braiding Funds. Registered Apprenticeship

Braiding Funds to Support Registered Apprenticeship Michigan Works! Annual Conference Mt. Pleasant, MI October 3, 2016 Today s Session Moderator: Marcia Black-Watson, Michigan Talent Investment Agency

Braiding Funds to Support Registered Apprenticeship Michigan Works! Annual Conference Mt. Pleasant, MI October 3, 2016 Today s Session Moderator: Marcia Black-Watson, Michigan Talent Investment Agency

Setting Up Tuition Controls, Criteria, Equations, and Waivers

Setting Up Tuition Controls, Criteria, Equations, and Waivers Understanding Tuition Controls, Criteria, Equations, and Waivers Controls, criteria, and waivers determine when the system calculates tuition

Setting Up Tuition Controls, Criteria, Equations, and Waivers Understanding Tuition Controls, Criteria, Equations, and Waivers Controls, criteria, and waivers determine when the system calculates tuition

6 Financial Aid Information

6 This chapter includes information regarding the Financial Aid area of the CA program, including: Accessing Student-Athlete Information regarding the Financial Aid screen (e.g., adding financial aid information,

6 This chapter includes information regarding the Financial Aid area of the CA program, including: Accessing Student-Athlete Information regarding the Financial Aid screen (e.g., adding financial aid information,

AGENDA ITEM VI-E October 2005 Page 1 CHAPTER 13. FINANCIAL PLANNING

Page 1 CHAPTER 13. FINANCIAL PLANNING Subchapter F. FORMULA FUNDING AND TUITION CHARGED FOR REPEATED AND EXCESS HOURS OF UNDERGRADUATE STUDENTS Section 13.100. Purpose. 13.101. Authority 13.102. Definitions.

Page 1 CHAPTER 13. FINANCIAL PLANNING Subchapter F. FORMULA FUNDING AND TUITION CHARGED FOR REPEATED AND EXCESS HOURS OF UNDERGRADUATE STUDENTS Section 13.100. Purpose. 13.101. Authority 13.102. Definitions.

REGULATIONS RELATING TO ADMISSION, STUDIES AND EXAMINATION AT THE UNIVERSITY COLLEGE OF SOUTHEAST NORWAY

REGULATIONS RELATING TO ADMISSION, STUDIES AND EXAMINATION AT THE UNIVERSITY COLLEGE OF SOUTHEAST NORWAY Authorisation: Passed by the Joint Board at the University College of Southeast Norway on 18 December

REGULATIONS RELATING TO ADMISSION, STUDIES AND EXAMINATION AT THE UNIVERSITY COLLEGE OF SOUTHEAST NORWAY Authorisation: Passed by the Joint Board at the University College of Southeast Norway on 18 December

Intellectual Property

Intellectual Property Section: Chapter: Date Updated: IV: Research and Sponsored Projects 4 December 7, 2012 Policies governing intellectual property related to or arising from employment with The University

Intellectual Property Section: Chapter: Date Updated: IV: Research and Sponsored Projects 4 December 7, 2012 Policies governing intellectual property related to or arising from employment with The University